In business, uncertainty is inevitable — whether it’s a customer who might default, a product warranty that may be claimed, or a lawsuit that could result in payment. Accounting standards recognize this uncertainty through provisioning, a process that ensures companies record anticipated expenses or losses before they actually occur.

Provisioning is a key part of prudent accounting, ensuring that financial statements reflect not only what has happened, but also what is likely to happen.

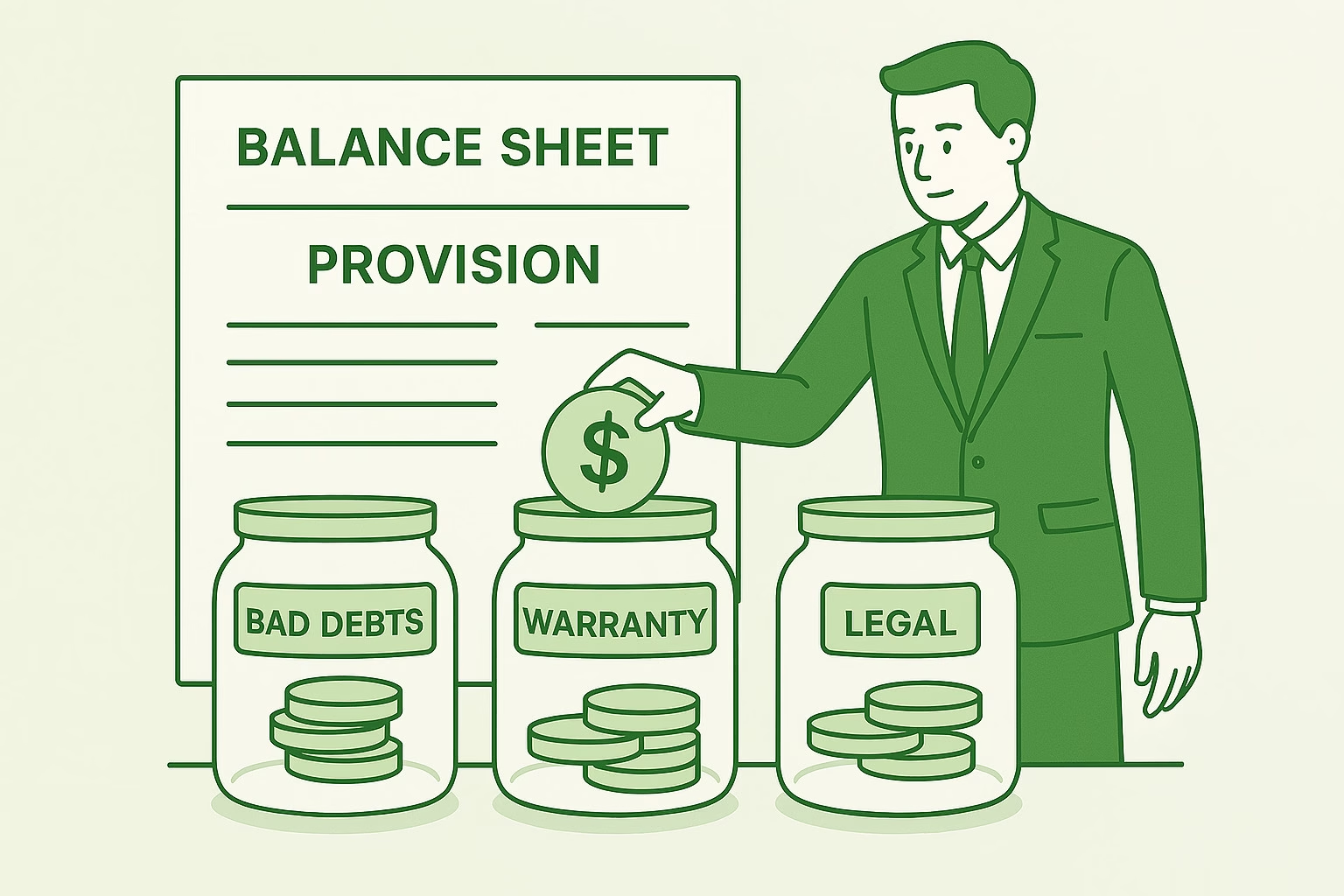

💡 What Is Provisioning?

Provisioning refers to the act of setting aside an estimated amount in the accounts for a probable future obligation or loss. It is based on the accounting principle of prudence (or conservatism) — the idea that potential losses should be recognized as soon as they are foreseeable, while potential gains are recognized only when realized.

A provision is recorded as a liability because it represents a present obligation that will probably require future outflow of resources (like cash or assets).

🧾 Common Types of Provisions

- Provision for Bad Debts (Doubtful Debts)

- Created when there’s uncertainty about collecting payments from customers.

- Ensures accounts receivable are shown at a realistic, recoverable amount.

- Provision for Warranties

- Companies selling goods with warranties must estimate future repair or replacement costs.

- Provision for Legal Claims

- If a company faces probable litigation losses, it sets aside a provision for potential settlement costs.

- Provision for Restructuring

- Created when a company has a formal plan to reorganize and will incur costs such as layoffs or asset write-downs.

- Provision for Decommissioning or Restoration

- Common in industries like oil, gas, and mining — where companies must restore sites at the end of use.

📊 Example

Suppose a company sells electronics with a one-year warranty.

- Based on historical data, 3% of sales typically result in warranty claims.

- If annual sales total $10 million, the expected warranty cost is $300,000.

Journal Entry:

| Account | Debit | Credit |

|---|---|---|

| Warranty Expense | 300,000 | |

| Provision for Warranty | 300,000 |

This provision ensures that the financial statements for the year include the estimated cost of honoring warranties, even before the claims occur.

⚖️ Recognition Criteria (IAS 37)

A provision should be recognized only when:

- The company has a present obligation (legal or constructive).

- It is probable that an outflow of resources will be required to settle it.

- A reliable estimate can be made of the amount.

If any of these conditions are not met, the obligation is disclosed as a contingent liability instead of being recognized as a provision.

💬 Why Provisioning Matters

- Ensures accuracy: Reflects true financial position and expected obligations.

- Prevents overstated profits: Recognizing future costs early keeps results realistic.

- Builds investor trust: Transparent provisioning practices demonstrate strong risk management.

- Required by standards: IFRS and GAAP both require provisions for probable and measurable obligations.

🧠 Simple Analogy

Think of provisioning like setting money aside for an upcoming repair you know is coming. You may not have the bill yet, but you recognize the expense now to be ready when it arrives.

🪙 Key Takeaway

Provisioning is about foresight — recognizing likely future costs today to present a truthful and cautious picture of financial health. It ensures that companies don’t overstate profits and remain prepared for uncertainties ahead.