Most SME owners encounter carbon accounting the same way — a large customer sends a sustainability questionnaire, or an accountant mentions the carbon tax, or a bank asks about ESG exposure before approving a facility. The first instinct is usually to assume it is something for bigger companies with dedicated sustainability teams. The second instinct, once you look into it, is that it is more manageable than it appeared.

Both instincts are right. Carbon accounting does originate from large-company frameworks designed for companies with the resources to staff entire ESG functions. But the fundamentals — what you actually need to measure, track, and report — translate down to SME scale without most of the complexity.

This post explains what carbon accounting is, what the three emission scopes mean in practice for an SME, and how to approach it realistically if you are starting from scratch.

Why This Is Becoming Relevant for Singapore SMEs Specifically

The pressure on SMEs to engage with carbon accounting is coming from several directions simultaneously, and it is more acute in Singapore than in many other markets.

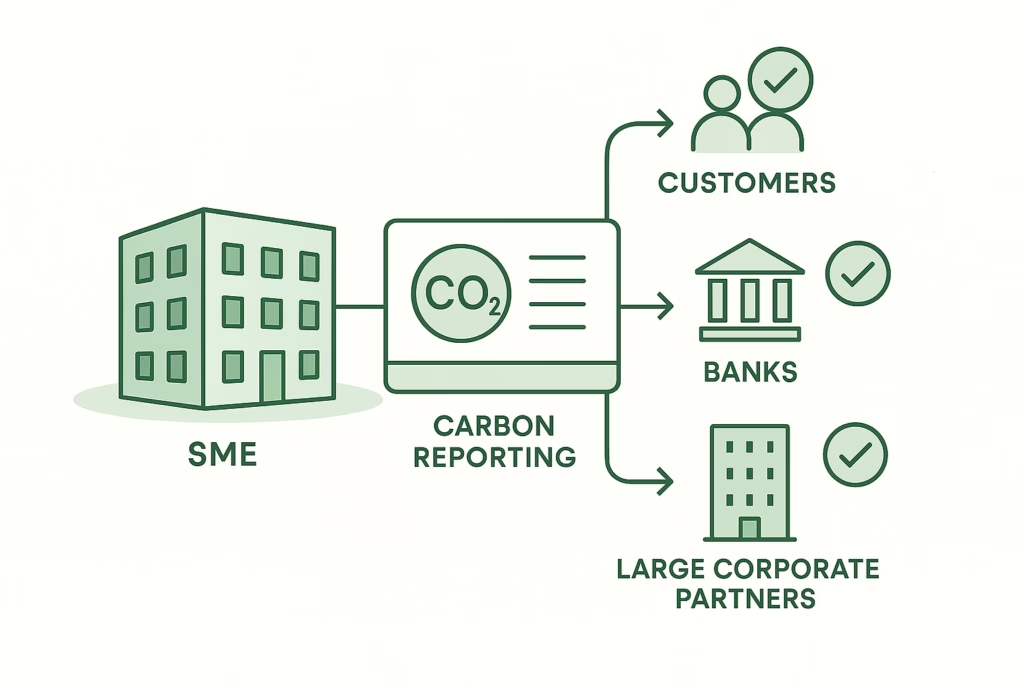

Singapore’s carbon tax applies directly to large emitters, but its downstream effects reach SMEs through supply chains. If your business supplies goods or services to a listed company or a multinational with sustainability reporting obligations, that company’s Scope 3 emissions include your emissions. Increasingly, procurement teams are asking suppliers to disclose carbon data as a condition of doing business — not as a future possibility, but as a current commercial requirement.

At the same time, Singapore’s carbon tax has been rising. It was S$5 per tonne of CO₂e until 2023, moved to S$25 in 2024, and is scheduled to reach S$45 in 2026 before climbing to between S$50 and S$80 by 2030. For SMEs that consume significant energy or operate energy-intensive processes, this trajectory has direct cost implications that are worth understanding now rather than absorbing as a surprise.

Banks and lenders are also beginning to factor climate risk into credit assessments, even for smaller businesses. SMEs that can demonstrate awareness of their emissions profile — and a credible approach to managing it — are better positioned than those who cannot.

The Three Scopes: What They Mean for a Typical SME

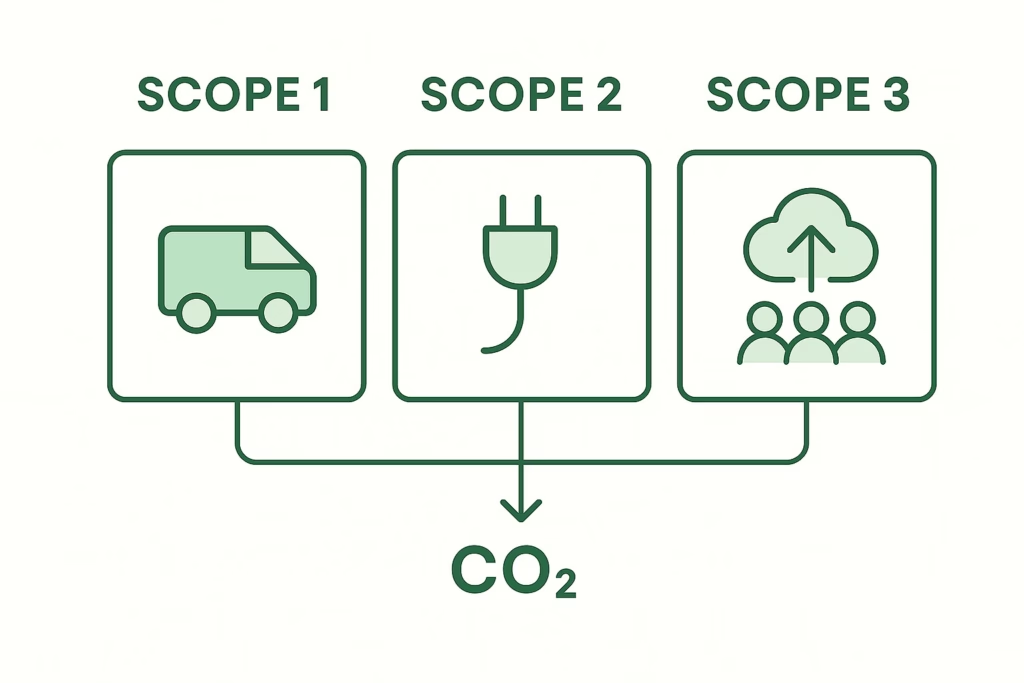

Carbon accounting uses the GHG Protocol framework, which divides emissions into three categories based on their source and your level of control over them.

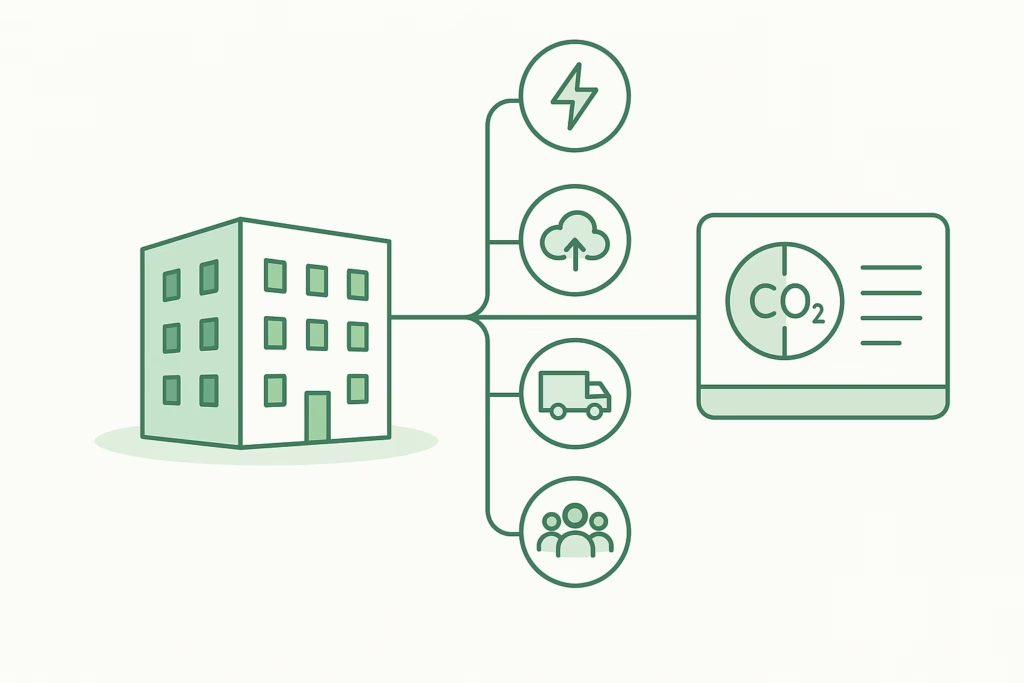

Scope 1 covers emissions that come directly from sources your business owns or controls — company vehicles, on-site combustion, fuel-powered equipment. For most service-based SMEs, Scope 1 is small. For businesses with a vehicle fleet, manufacturing equipment, or on-site generators, it can be material.

Scope 2 covers the emissions associated with the electricity and energy you purchase. Every kilowatt-hour of electricity drawn from the grid has a carbon intensity determined by how that electricity was generated. For most SMEs, Scope 2 is the most straightforward starting point: the data already exists in your utility bills, and the calculation method is well-established. Singapore’s grid emission factor is published by the Energy Market Authority and updated regularly.

Scope 3 covers everything else — emissions that occur in your value chain but outside your direct control. This includes the emissions embedded in goods and services you purchase, business travel, logistics, employee commuting, and cloud or SaaS usage. Scope 3 is typically the largest category, and also the hardest to measure precisely. For SMEs, the practical approach is to identify the two or three Scope 3 categories most material to your business and start there, rather than attempting a complete inventory on day one.

What Carbon Accounting Actually Involves

The mechanics are more familiar than most SME owners expect. You identify which emission sources are relevant to your business. You collect the underlying activity data — electricity consumption in kWh, fuel in litres, travel distances, spend with key suppliers. You apply published emission factors, which convert activity data into CO₂e figures. Then you aggregate the results by scope and period.

Most SMEs already hold the activity data they need in their accounting system, expense reports, and utility accounts. The missing piece is typically the emission factors and the structure to apply them consistently. Modern carbon accounting tools handle this, and the entry-level options are affordable.

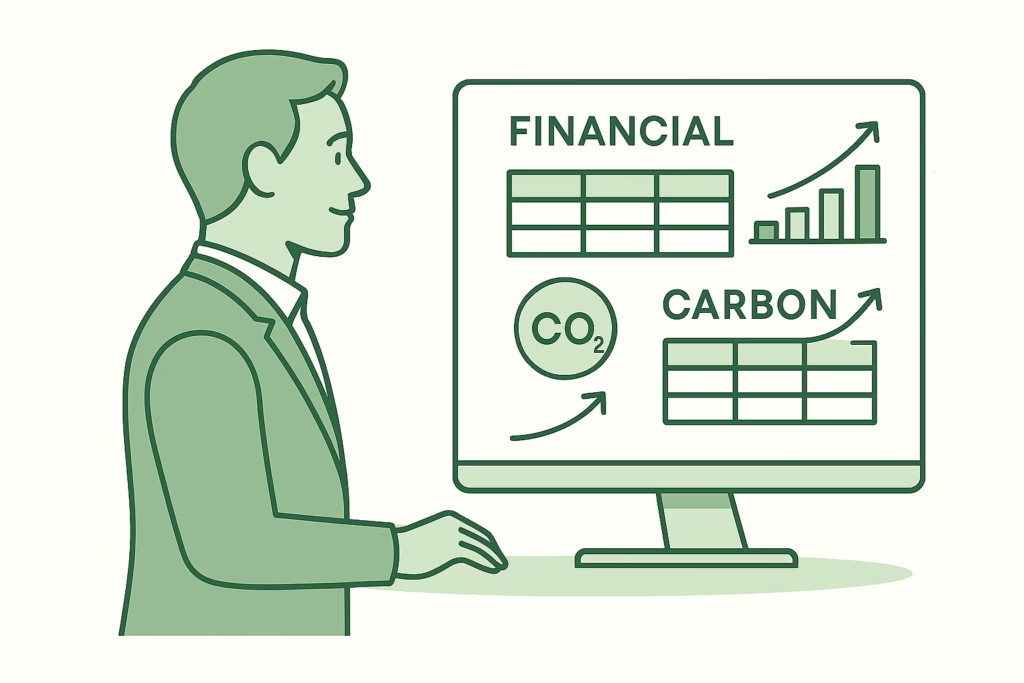

The output — a carbon footprint statement, structured by scope — mirrors a financial report in form. It covers a defined period, reports a quantified outcome, is traceable back to source data, and can be compared period over period to assess whether the trajectory is moving in the right direction. SMEs with a clear financial reporting process generally find the conceptual transition to carbon reporting more intuitive than they expected.

A Realistic Starting Point

For an SME approaching carbon accounting for the first time, the practical sequence is: start with Scope 2, add the most significant Scope 1 sources if applicable, and then layer in two or three Scope 3 categories — typically the ones your customers or lenders are most likely to ask about. Use estimates where precise data is not available. The goal in year one is a credible, documented baseline, not a perfectly complete inventory.

Improve the data quality and coverage in subsequent years. Carbon accounting, like financial reporting, matures as the business invests in better data collection and processes.

Where Financial Reporting and Carbon Reporting Intersect

One practical implication for SMEs that already have a structured financial reporting process is that the two disciplines increasingly overlap. ESG-aware lenders and investors want to see financial data and sustainability data in the same review. Supply chain questionnaires often ask for revenue context alongside emission figures. Boards and management teams want to understand carbon cost exposure alongside operational cost trends.

For multi-entity groups, this creates a consolidation challenge that mirrors the financial one: emissions data from different entities needs to be aggregated and reported at the group level, just as financial data does. The data structures, review processes, and reporting cadence that a finance team uses for consolidated financial reporting are directly transferable to consolidated emissions reporting.

If your business already manages multi-entity financial consolidation through BrizoConsol, the same structured approach — entity-level data, common categorisation, group-level aggregation — applies to building a carbon reporting process that scales with the group.

The Practical Takeaway

Carbon accounting is becoming a business requirement for Singapore SMEs, not because of direct regulatory obligation for most, but because of the indirect pressure from supply chains, lenders, and the rising cost of carbon-intensive operations. The businesses that build a baseline now are better positioned — commercially and operationally — than those that engage only when the pressure becomes unavoidable.

The process is less complex than it initially appears. The data you need mostly exists already. The framework is established. Starting small and improving over time is more valuable than waiting until you can do it perfectly.

To see how BrizoConsol supports structured financial reporting for multi-entity SMEs — the foundation that makes integrating carbon and financial data manageable — visit brizoconsol.com/see-it-in-action.

BrizoSystem is the company behind BrizoConsol, a multi-entity financial consolidation and reporting platform for accounting firms and finance teams. BrizoConsol integrates with Xero, QuickBooks, MYOB, and Zoho Books.