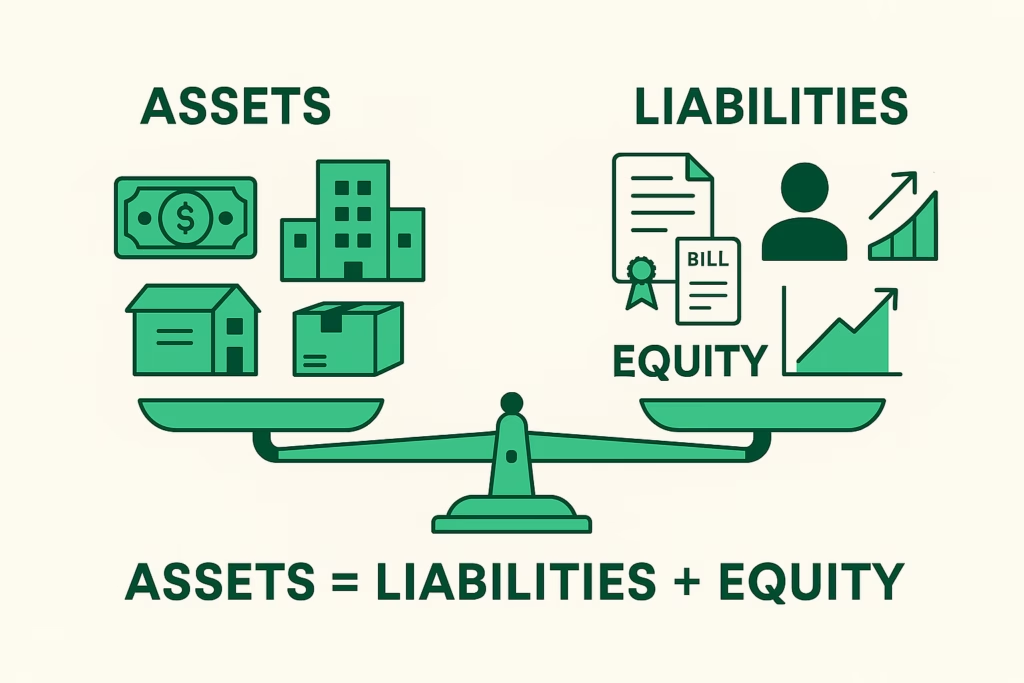

The accounting equation is the foundational rule that every financial statement is built on. It states that the total resources a business controls must equal the total claims on those resources — from lenders and from owners.

Assets = Liabilities + Equity

No transaction can be recorded in a way that breaks this equation. Every entry in the accounting system has a debit and a credit of equal amount, which ensures the equation remains in balance at all times. This is the mechanical basis of double-entry accounting, and it is also the conceptual basis of the balance sheet.

The Three Components

Assets

Assets are resources controlled by the entity from which future economic benefits are expected to flow. They are everything the business owns or has rights to — cash, receivables, inventory, property, equipment, intangibles. Assets are classified as current (convertible to cash or consumed within 12 months) or non-current (held for longer-term use or investment).

Liabilities

Liabilities are present obligations arising from past events — amounts owed to external parties that will require a future outflow of economic resources. They include trade payables, bank loans, accrued expenses, tax liabilities, and provisions. Like assets, liabilities are classified as current (due within 12 months) or non-current.

Equity

Equity is the residual interest in the assets of the entity after deducting all liabilities — the owners’ claim. It includes the original capital contributed by shareholders, accumulated profits retained in the business (retained earnings), and other comprehensive income items such as revaluation surpluses and currency translation adjustments. Equity grows when the business is profitable and declines when it makes losses or pays dividends.

How the Equation Stays in Balance

Every transaction simultaneously affects at least two accounts in a way that keeps the equation balanced. This is the double-entry principle.

Transaction 1 — purchase equipment with cash ($80,000)

| Account | Debit | Credit | Effect on equation |

|---|---|---|---|

| Equipment (asset) | $80,000 | Assets +$80k | |

| Cash (asset) | $80,000 | Assets −$80k |

Net effect: two assets change in opposite directions. Total assets unchanged. Equation still balanced.

Transaction 2 — take out a bank loan ($200,000)

| Account | Debit | Credit | Effect on equation |

|---|---|---|---|

| Cash (asset) | $200,000 | Assets +$200k | |

| Bank Loan (liability) | $200,000 | Liabilities +$200k |

Net effect: assets and liabilities both increase by the same amount. Equation remains balanced.

Transaction 3 — record net profit of $50,000 for the period

| Account | Debit | Credit | Effect on equation |

|---|---|---|---|

| Revenue and expense accounts (P&L) | $50,000 net | — | |

| Retained Earnings (equity) | $50,000 | Equity +$50k |

Net effect: equity increases. This is matched by the net increase in assets that the profitable trading generated. Equation balanced.

What the Equation Reveals About Financial Health

The equation’s components and their relative proportions tell you a great deal about how a business is financed and how much financial risk it carries.

- Leverage: If liabilities are large relative to equity, the business is heavily debt-financed. Lenders and creditors have more claim on the assets than the owners do. A common metric — debt-to-equity ratio (liabilities / equity) — measures this directly.

- Net assets: Equity = Assets − Liabilities. This is the business’s net asset value — what would theoretically be left for shareholders if all assets were sold and all liabilities settled at carrying value. A negative equity position means liabilities exceed assets — a sign of financial distress.

- Working capital: Current assets minus current liabilities is the working capital — the liquid buffer the business has to meet short-term obligations. A business with strong profits but negative working capital may still face a cash crisis if its short-term liabilities exceed its liquid assets.

The Equation in a Consolidated Balance Sheet

In a group with multiple entities, the consolidated balance sheet still follows the same equation — but the components are materially different from simply adding up the entity balance sheets. The consolidation process produces three changes that the equation must accommodate:

Intercompany eliminations reduce both assets and liabilities. Intercompany receivables (assets in one entity) and the corresponding payables (liabilities in another) are eliminated on consolidation. Both sides are removed. The equation stays balanced because equal amounts are removed from both assets and liabilities simultaneously.

Goodwill appears as an asset. When a subsidiary is acquired at a price above the fair value of its identifiable net assets, the difference is recognised as goodwill — an asset in the consolidated balance sheet that does not appear in any entity’s own accounts. The offsetting entry is to the retained earnings or investment elimination. The equation is maintained because the acquisition eliminates the investment in subsidiary (an asset in the parent) and recognises goodwill plus the subsidiary’s net assets in its place.

Equity includes non-controlling interests. In a partially-owned subsidiary, not all equity belongs to the parent. The consolidated equity is split between the parent’s shareholders and the non-controlling interests (NCI) — minority shareholders who have a claim on the subsidiary’s net assets. The NCI is recognised within equity as a separate component, not as a liability.

Consolidated balance sheet — simplified Group consolidated balance sheet after eliminations:

Assets: External assets only (intercompany receivables eliminated) + Goodwill

Liabilities: External liabilities only (intercompany payables eliminated)

Equity: Parent shareholders’ equity + NCI equity + CTA (from foreign subsidiaries)

Assets still equal Liabilities plus Equity. The components are different from any individual entity, but the equation is unchanged.

For multi-entity groups, producing a consolidated balance sheet that correctly reflects the accounting equation — with eliminations, goodwill, NCI, and foreign currency translation all applied — is the core function of BrizoConsol. Learn more or see it in action →