Latest blogs

-

Your Legal Structure Is Not Your Management Structure — Here’s How to Consolidate for Both

Most group finance teams run into the same problem eventually. The legal structure of the business — the holding company, its subsidiaries, the ownership percentages — reflects how the group was built, not necessarily how it should be managed. A regional CFO wants to see APAC performance as a single view. A board wants to…

-

New Feature in BrizoConsol: Define Ownership Percentage and Calculate Non-Controlling Interest (NCI)

Managing the financials of a complex group structure can be challenging, especially when ownership percentages vary across subsidiaries. To make this process more intuitive and accurate, BrizoConsol has introduced a powerful new feature that allows users to define ownership percentages for each organization within their group. This feature automatically calculates Non-Controlling Interest (NCI) for both…

-

The Hidden Costs of Using Excel for Multi-Company Consolidation

Excel is a legitimate starting point for multi-company consolidation. At two entities with straightforward intercompany flows and no foreign currency, a well-maintained spreadsheet model is reasonable. The problem is that Excel’s costs accumulate gradually — each entity added, each currency introduced, each new intercompany relationship — until the point where the model is holding the…

-

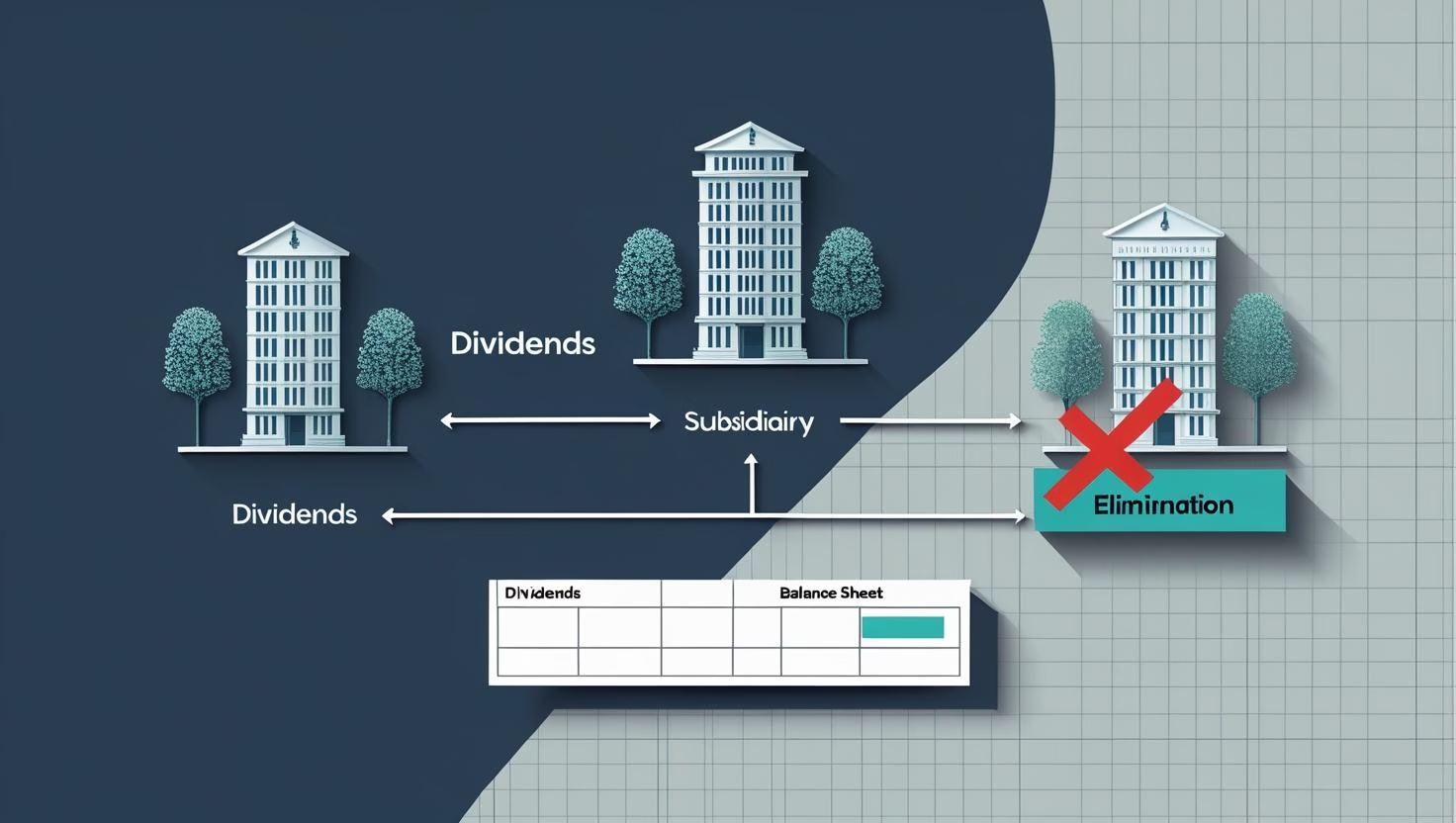

Understanding Intercompany Dividend Elimination in Financial Consolidation

Intercompany dividend elimination is one of the most commonly mishandled adjustments in group financial consolidation. When a subsidiary pays a dividend to its parent or another group entity, both sides record the transaction — but from a consolidated perspective, the money never left the group. If those entries aren’t eliminated, the group’s income and retained…

-

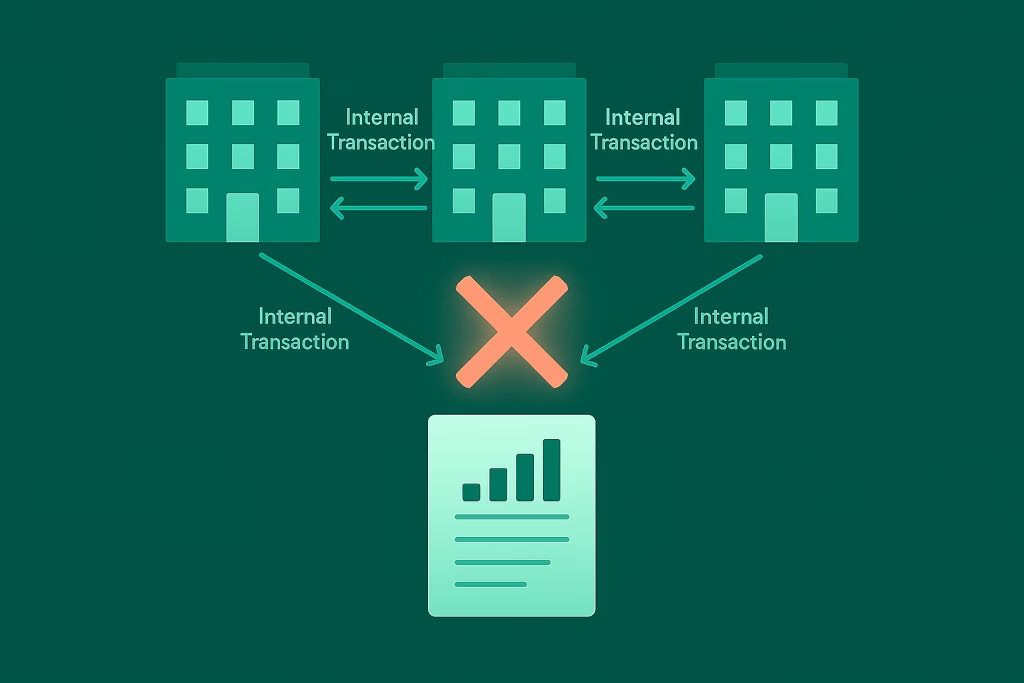

Why Do We Eliminate Intercompany Transactions in Financial Consolidation?

Seeing the Group as One When a group of companies is under common control—such as a parent company with several subsidiaries—the goal of financial consolidation is to present their financials as if they were one single economic entity. This means transactions between the entities in the group are internal, not external, and do not represent…