The deal is signed. The acquisition is complete. And now the finance team is handed the hard part: integrating the newly acquired entity into the group’s consolidation — on a platform it didn’t design, using data from an accounting system it may have never seen before, on a timeline driven by the next month-end close.

Without a structured onboarding process, the result is unreliable consolidated reports and a finance team buried in reconciliation work precisely when stakeholders are most eager to see how the acquisition is performing. This guide covers the five steps to onboard a newly acquired entity cleanly — from first data connection to validated consolidated report.

Before You Start: Fix the Acquisition Date

Under IFRS 3, the entity enters the consolidation from the acquisition date — the date on which control passes, which may differ from the legal completion date or the date funds were transferred. Revenue, expenses, assets, and liabilities of the acquired entity are consolidated from that date only. Getting the acquisition date wrong shifts income and costs between periods and misstates goodwill.

Confirm the acquisition date before configuring anything else. It determines the opening balance sheet at fair value, the period from which results are consolidated, and the starting point for PPA amortisation and NCI calculations.

Step 1: Connect the Entity’s Accounting Software

Confirm which system the acquired entity uses — Xero, QuickBooks, MYOB, Zoho Books, or another platform — and secure administrative credentials. This access request should go out on day one: the acquired entity’s finance team may have changed, credentials may sit with a third-party bookkeeper, or the software subscription may still be in the previous owner’s name. Delays here push every subsequent step back.

Once access is confirmed, BrizoConsol connects via API directly to the accounting system, pulling the trial balance, P&L, and balance sheet in real time. From the point of connection, BrizoConsol shows both your existing group and the new entity side by side — without anyone manually exporting a spreadsheet. As the entity’s finance team continues processing transactions during the integration period, the consolidated view stays current automatically.

For entities on desktop or legacy systems without API access, BrizoConsol accepts a structured Excel import from a standardised trial balance template.

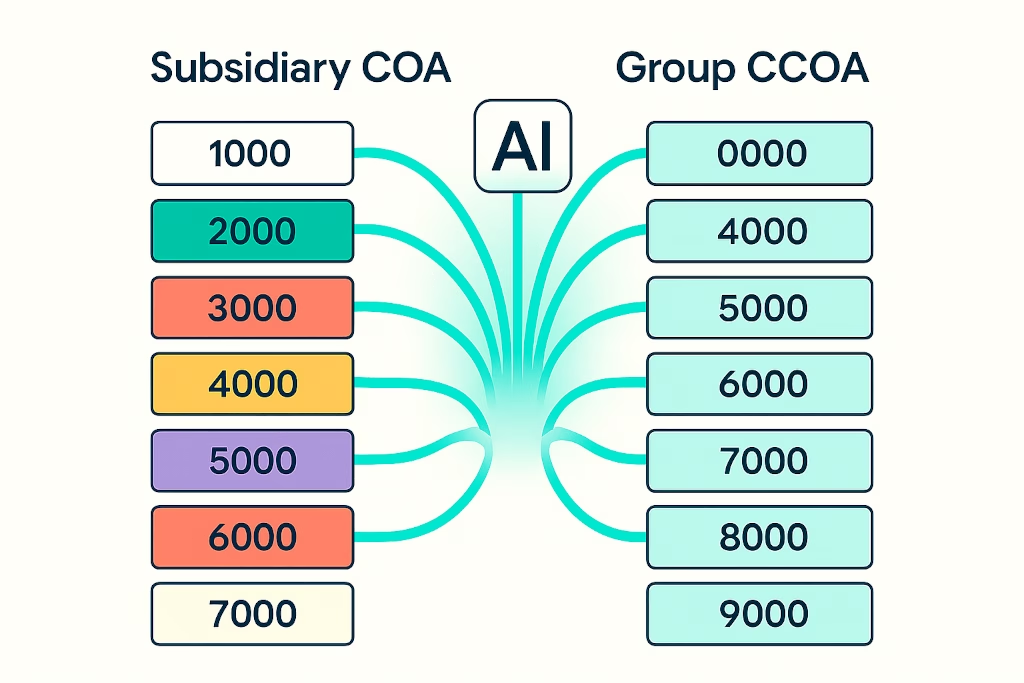

Step 2: Map the Chart of Accounts to Your Group COA

Almost every acquired entity uses a different chart of accounts — different codes, different naming conventions, different granularity. Before the entity’s figures can appear meaningfully in consolidated statements, its accounts must be mapped to the group’s Common Chart of Accounts (CCOA).

BrizoConsol’s AI-assisted mapping analyses the acquired entity’s account names and structures and proposes mappings to the group CCOA automatically. Finance teams typically find 80–90% of mappings correctly proposed on the first pass, with a small number of edge cases to review and confirm. The mapping lives in the platform — not in a separate spreadsheet — and updates automatically as new accounts are added in the entity’s accounting system.

Before finalising the mapping, involve the acquired entity’s finance team or accountant. They understand the intent behind ambiguous account categorisations — particularly items like depreciation split by asset class, cost of goods vs operating expenses, or local tax accounts — that may not be obvious from account names alone.

💡 New accounts after onboarding: Configure an unmapped account alert so that whenever the entity’s finance team adds a new account in their system, BrizoConsol flags it before the next consolidation run. Unmapped accounts silently drop from the consolidated statements without this check.

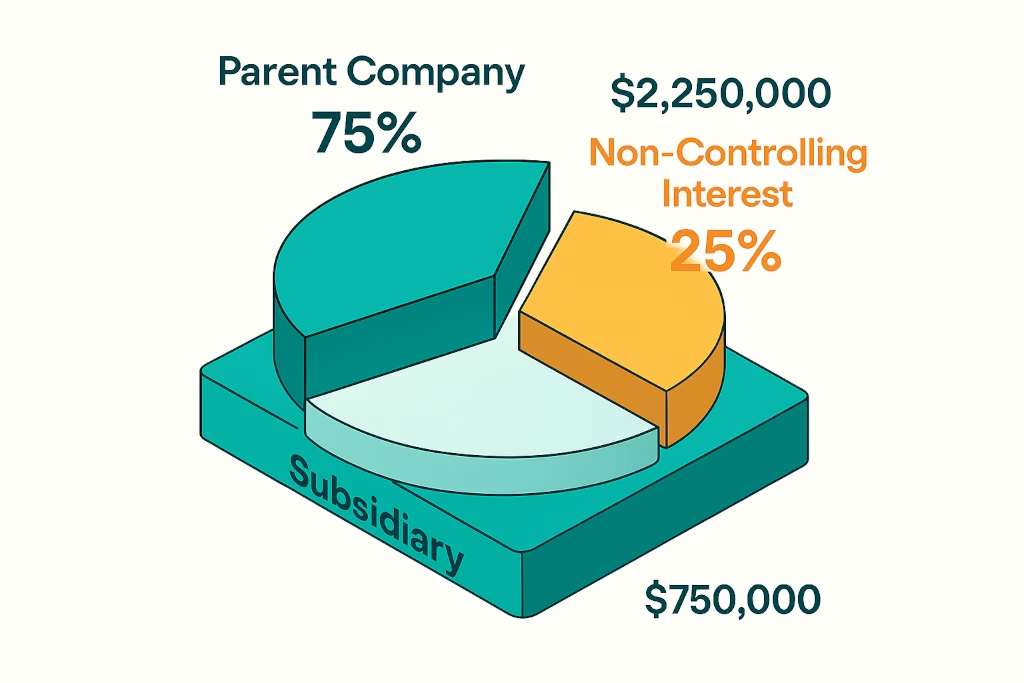

Step 3: Set Ownership, Configure NCI, and Record the PPA

Ownership configuration is the most consequential setting to get right. If the group acquired 100% of the entity, setup is straightforward. For partial acquisitions — 80%, 70%, 51% — the remaining percentage belongs to minority shareholders whose interest must be disclosed separately as NCI in the consolidated statements. In BrizoConsol, ownership percentages are set at the entity level and NCI is calculated and presented automatically once the percentage is defined.

At the same time, the purchase price allocation (PPA) must be completed. IFRS 3 requires that the identifiable assets and liabilities of the acquired entity are measured at fair value at the acquisition date, with any excess of consideration over net fair value recognised as goodwill. Until the PPA is completed:

- Goodwill cannot be correctly determined

- PPA intangibles (customer relationships, trade names, technology) are missing from the consolidated balance sheet

- PPA amortisation — which exists only at the consolidation level, not in the entity’s own books — cannot be applied

- The deferred tax liability on fair value uplifts has not been recognised

IFRS 3 allows a 12-month measurement period to finalise the PPA. Provisional amounts can be used in the interim, but the entity should not be onboarded as if the book value of its net assets equals the fair value.

🚩 The most common PPA omission: Onboarding the acquired entity at its pre-acquisition book values without recording provisional PPA fair values. The entity enters the consolidation showing the net book value of its assets — not their acquisition-date fair value — producing a materially incorrect consolidated balance sheet from day one.

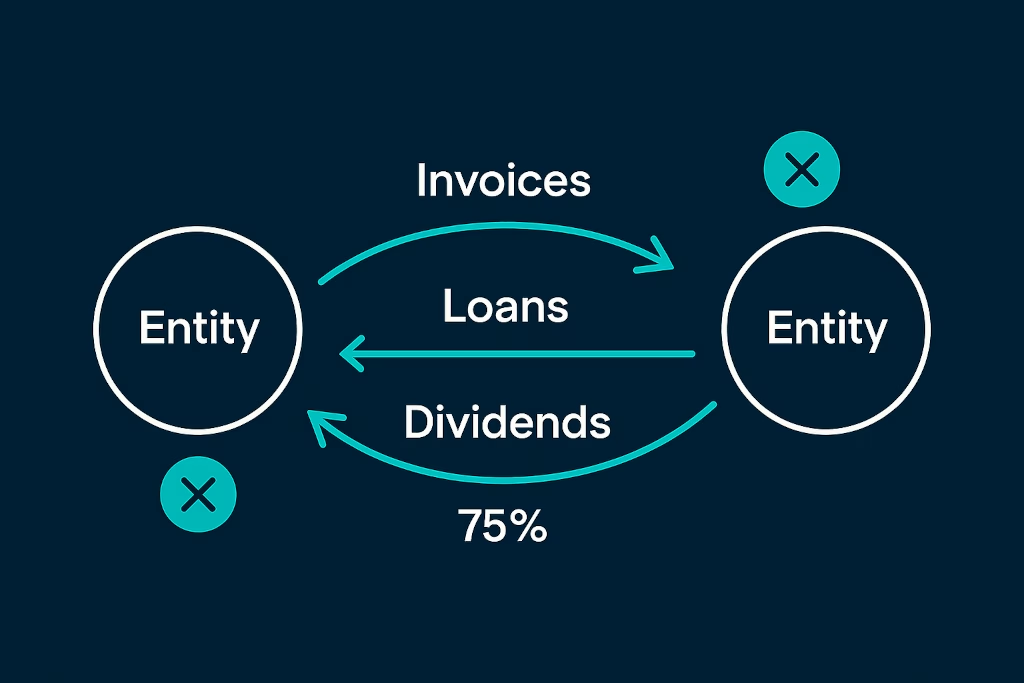

Step 4: Define Intercompany Relationships and Elimination Rules

Identify which intercompany transactions will need to be eliminated — both those that exist at acquisition date and those being established as part of the post-acquisition integration. Common ones to configure immediately:

- Management fees: Where the group charges the acquired entity for shared services, brand management, or group finance

- Working capital loans: Where the parent has funded the acquisition through intercompany lending; the loan receivable (parent) and payable (entity) must be eliminated, along with the associated interest

- Supply relationships: Where the acquired entity buys from or sells to other group entities — intercompany revenue and cost, plus any unrealised profit on goods not yet sold externally

- Pre-existing relationships: Any balances that existed between the acquired entity and the group before the acquisition must be assessed — they may qualify as settlement of pre-existing relationships under IFRS 3

In BrizoConsol, intercompany relationships are configured at the entity level and elimination entries are applied automatically each period — including FX-aware eliminations where the entities operate in different currencies.

Step 5: Run the First Consolidated Report and Validate

With data connected, accounts mapped, ownership set, PPA recorded, and intercompany relationships configured, run the first consolidated report including the new entity. Treat this as a validation exercise before it goes anywhere near the board.

Specific checks to run:

- Entity revenue contribution: Does the entity’s contribution to group revenue match the expected post-acquisition period? (Only from acquisition date, not the full year.)

- NCI balance: Is the NCI equity balance reasonable given the ownership percentage and the entity’s net assets at acquisition?

- Intercompany netting: Do intercompany receivables and payables net to zero across the group after elimination?

- Goodwill: Does goodwill on the consolidated balance sheet match the PPA calculation?

- Opening balance: Does the entity’s opening balance sheet in the consolidation agree to the acquisition-date fair values from the PPA?

BrizoConsol’s entity-level drill-down lets you click into any line in the consolidated report and trace it back to the entity and account behind it — making these checks fast rather than requiring a separate manual investigation.

Onboarding a newly acquired entity into BrizoConsol takes days, not weeks — with API connection, AI-assisted account mapping, NCI configuration, and intercompany elimination rules all managed in the same platform. Learn more or see it in action →