Intercompany loans are a common financing tool within corporate groups. A parent may lend funds to a subsidiary, or two subsidiaries may arrange a loan between themselves. On the surface, these transactions provide flexibility in managing liquidity across the group. But when it comes to preparing consolidated financial statements, these loans — along with the interest income and expense they generate — must be eliminated.

Why? Because they do not represent external transactions. From the perspective of the group as a whole, you cannot owe money to yourself, nor can you generate interest income internally. Eliminating these balances is critical for presenting a true and fair view of the group’s financial position and performance.

This guide provides a deep dive into the types of intercompany loans, how interest is handled, common challenges, and a step-by-step process for eliminating them.

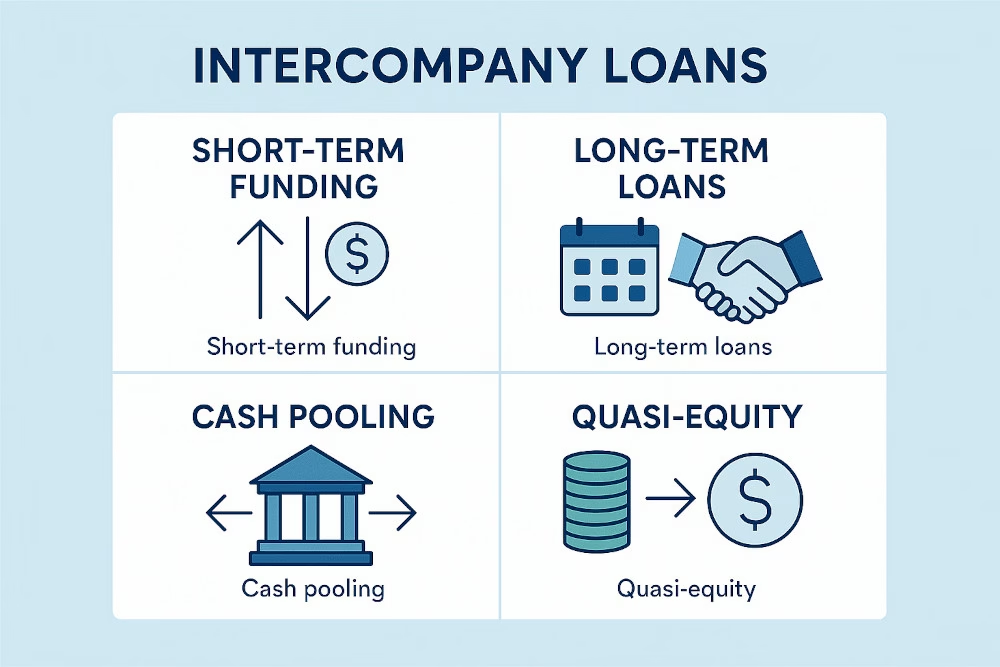

Types of Intercompany Loans

Not all intercompany loans are the same. They can differ in purpose, terms, and accounting treatment. Below are the most common types:

1. Short-Term Funding Arrangements

These are temporary loans used to manage working capital or liquidity shortfalls — for example, a parent advancing funds to a subsidiary at month-end to cover payroll or supplier payments. Because they are short in duration, they often appear and disappear within a single reporting period.

At consolidation, the loan receivable on the parent’s balance sheet and the corresponding loan payable on the subsidiary’s balance sheet cancel each other out. Any interest charged during the period must also be eliminated from both the income statement and, if accrued, the balance sheet.

2. Long-Term Intercompany Loans

These are structured loans with longer repayment horizons, often carrying interest at market rates or transfer-pricing compliant rates. They are commonly used as an alternative to issuing additional equity, particularly where the lending entity has surplus cash and the borrowing entity needs capital without diluting ownership.

At consolidation, both the outstanding principal balances and all accumulated interest income and expense are eliminated. If the loan has been partially repaid, only the outstanding balance at the reporting date needs to be cancelled.

3. Cash Pooling Arrangements

In centralised treasury models, cash is pooled across group entities through a header account — typically held by a treasury entity or the parent. Entities with surpluses lend into the pool; entities with shortfalls draw from it. This optimises group-wide liquidity and reduces the need for external borrowing.

At consolidation, the result is numerous small intercompany receivables and payables across all participating entities, all of which must be eliminated. What remains after elimination is only the group’s net external borrowing position — which is the number that matters to external lenders and analysts.

4. Quasi-Equity Loans

Some intercompany loans are structured without fixed repayment terms, subordinated to other creditors, and in substance function more like equity than debt. Under IFRS 9, these instruments may need to be reclassified as equity before the elimination entry is posted.

The consolidation treatment depends on that classification decision. If reclassified as equity, the loan is eliminated against the subsidiary’s equity balance rather than against a loan payable. Groups should have a clear written policy defining the criteria for quasi-equity classification and apply it consistently across all entities and reporting periods.

5. Intercompany Interest Income and Expense

Regardless of loan type, whenever one entity charges interest on an intercompany loan, the lender records interest income and the borrower records interest expense. From the group’s perspective, this is a circular flow — the group cannot earn interest from itself. Both the income and the expense must always be eliminated, even if the principal loan balance has already been repaid.

Interest accruals that remain unpaid at period end — recorded as accrued income by the lender and accrued expense by the borrower — must also be eliminated from the consolidated balance sheet.

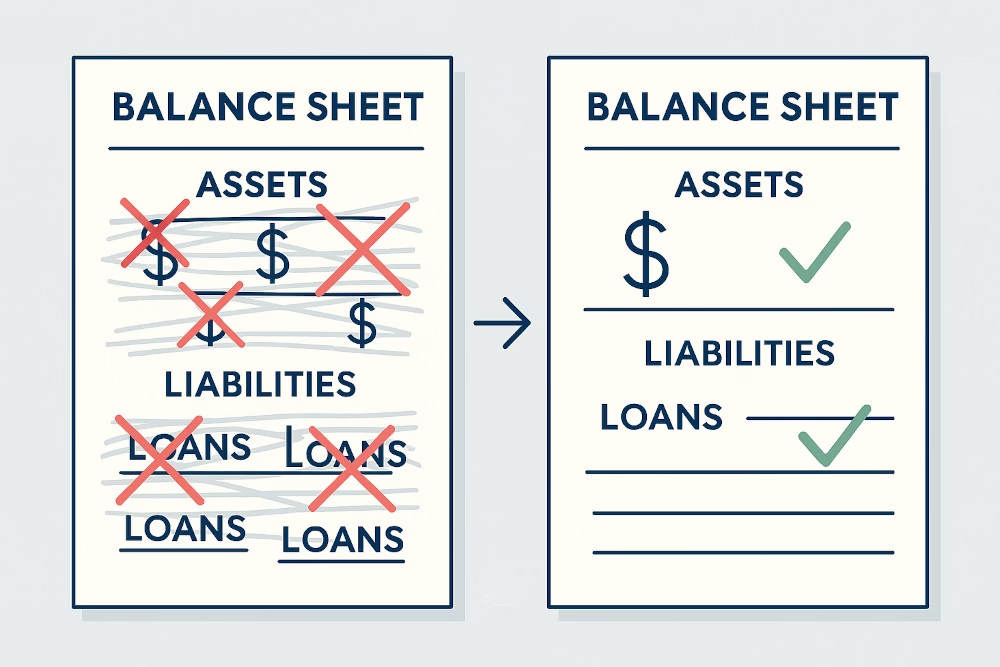

Why Elimination Is Necessary

Without elimination:

- Balance Sheet distortion → Assets (loan receivable) and liabilities (loan payable) are overstated.

- P&L distortion → Group revenue (interest income) and expenses (interest expense) are overstated.

- Ratios misrepresented → Debt-to-equity ratios and profitability measures are artificially skewed.

The consolidated financial statements should reflect only transactions with third parties, not internal activities.

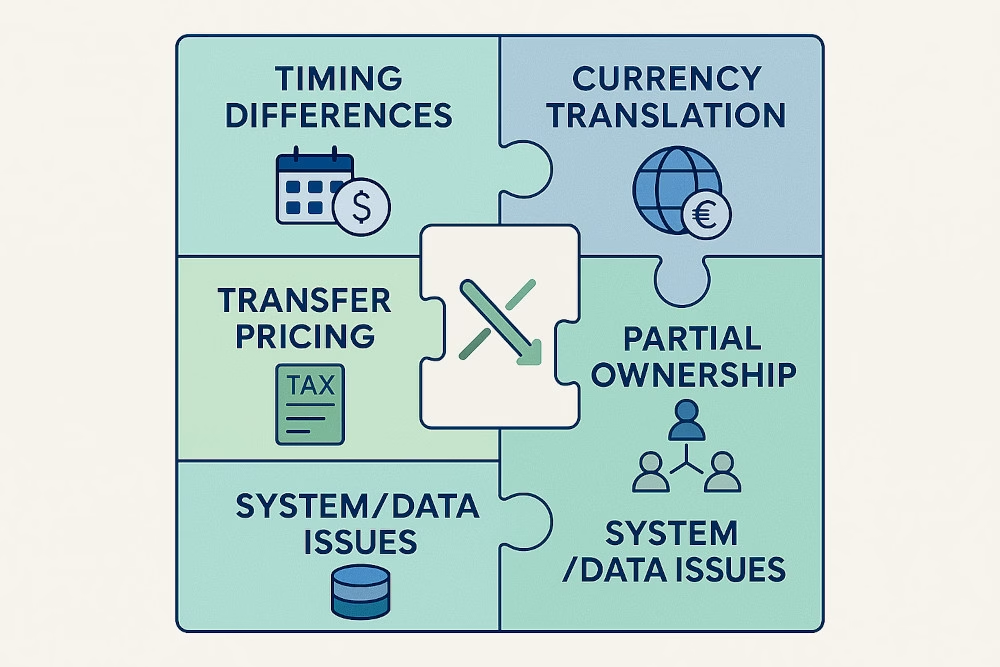

Common Challenges in Eliminating Intercompany Loans

- Timing Differences

- One entity records the loan in January, but the counterparty books it in February.

- Leads to mismatched balances.

- Currency Translation

- Loans denominated in foreign currencies create FX gains/losses in individual books.

- These must also be eliminated in consolidation.

- Transfer Pricing Compliance

- Loans must be at arm’s length. Eliminating interest does not eliminate the need for documentation and compliance with tax authorities.

- Partial Ownership

- If a subsidiary is not 100% owned, eliminations affect non-controlling interests.

- Interest elimination reduces the share of profit available to NCI.

- System and Data Issues

- Manual consolidations often result in mismatches between counterparties due to differences in GL coding, cut-offs, or reporting processes.

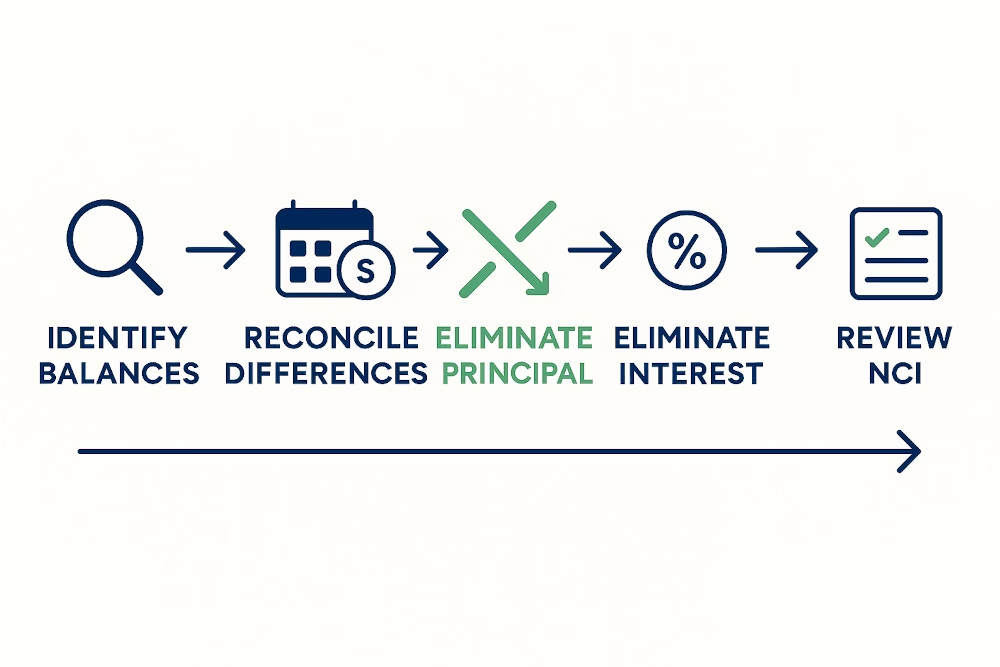

Step-by-Step Process to Eliminate Intercompany Loans and Interest

Step 1: Identify Intercompany Loan Balances

- Extract intercompany receivables/payables from the trial balance of each entity.

- Match counterparties, currencies, and terms.

Example:

- Parent Co. shows a loan receivable of $5M from Subsidiary A.

- Subsidiary A shows a loan payable of $5M to Parent Co.

- These must cancel in consolidation.

Step 2: Reconcile Differences

- Ensure loan balances match in both entities’ books.

- If differences arise due to FX, timing, or errors, adjustments must be made.

Detailed Example:

- Parent books loan on Jan 1 at $5M.

- Subsidiary records on Jan 2 at $4.95M due to FX.

- In consolidation, a $50K adjustment is required to align.

Step 3: Eliminate Principal Balances

| Account | Debit | Credit |

|---|---|---|

| Intercompany Loan Payable (Subsidiary A) | $5,000,000 | |

| Intercompany Loan Receivable (Parent Co.) | $5,000,000 |

Net impact: The consolidated balance sheet shows only the group’s external debt obligations — the internal loan disappears entirely.

Step 4: Eliminate Interest Income/Expense

| Account | Debit | Credit |

|---|---|---|

| Interest Income (Parent Co.) | $250,000 | |

| Interest Expense (Subsidiary A) | $250,000 |

Net impact: The consolidated P&L reflects only interest paid to external lenders. The group’s interest coverage ratios and profitability metrics are no longer distorted by internal financing charges.

If interest has been accrued but not yet paid at period end:

| Account | Debit | Credit |

|---|---|---|

| Accrued Interest Payable (Subsidiary A) | $250,000 | |

| Accrued Interest Receivable (Parent Co.) | $250,000 |

Step 5: Address FX Gains/Losses

When an intercompany loan is denominated in a currency different from one or both entities’ functional currencies, exchange rate movements between the loan origination date and the reporting date create FX differences. Under IAS 21, these are recognised as gains or losses in each entity’s individual accounts — but at group level, they are internal and must be eliminated.

Example: Parent Co. (USD functional) lends £3,000,000 to Subsidiary B (GBP functional). At loan origination, the rate is 1.25, so Parent records a $3,750,000 receivable. By reporting date the rate has moved to 1.20, so the receivable is now worth $3,600,000 — a $150,000 FX loss in Parent’s books. Subsidiary B still records £3,000,000 on its side. The $150,000 difference must be eliminated at consolidation:

| Account | Debit | Credit |

|---|---|---|

| Intercompany Loan Payable (Subsidiary B — translated) | $3,600,000 | |

| FX Loss — Consolidation Elimination | $150,000 | |

| Intercompany Loan Receivable (Parent Co.) | $3,750,000 |

Exception — Quasi-equity loans: Under IAS 21 paragraph 32, if an intercompany loan is in substance part of the net investment in a foreign operation (i.e. quasi-equity), FX differences are not taken to the P&L. Instead they are recognised in Other Comprehensive Income (OCI) and accumulated in the Currency Translation Reserve — and remain there until the foreign operation is disposed of.

Step 6: Review NCI Impact

When a subsidiary is not 100% owned, the interest elimination affects how profit is split between the parent and the non-controlling interest (NCI). Eliminating interest expense from the subsidiary’s P&L increases its reported profit — which means the NCI’s share of profit also increases proportionally.

Example: Parent owns 70% of Subsidiary A. Subsidiary A pays $250,000 interest to Parent on an intercompany loan. After elimination, Subsidiary A’s profit increases by $250,000. The NCI (30%) is entitled to 30% of that increase — an additional $75,000 allocated to NCI in the consolidated income statement.

| Without elimination | With elimination |

|---|---|

| Subsidiary A profit: $800,000 | Subsidiary A profit: $1,050,000 |

| NCI share (30%): $240,000 | NCI share (30%): $315,000 |

| Parent share (70%): $560,000 | Parent share (70%): $735,000 |

Finance teams must ensure their consolidation system allocates the elimination impact correctly between parent equity and NCI — not simply apply a 100% elimination that ignores the minority interest.

Best Practices for Managing Intercompany Loan Eliminations

- Automate Matching

- Use consolidation systems that auto-match intercompany balances, reducing manual reconciliations.

- Standardize Processes

- Require consistent GL codes for intercompany loans and interest.

- Align cut-off dates for month-end closing.

- Regular Reconciliations

- Perform intercompany reconciliations monthly, not just at year-end.

- Resolve mismatches proactively.

- Document Transfer Pricing

- Even though interest is eliminated in consolidation, maintain transfer-pricing support for tax compliance.

- Clear Policies for Quasi-Equity

- Define criteria for when intercompany loans should be treated as equity.

- Communicate these policies across the group.

- Audit Trail

- Maintain clear elimination entries for auditors, showing counterparties, amounts, and rationale.

How BrizoSystem Handles Intercompany Loan Eliminations

The challenges outlined in this guide — timing differences, FX mismatches, quasi-equity classification, cash pooling complexity, and NCI allocation — are exactly the scenarios where manual consolidation breaks down fastest. Each adds a layer of judgement and calculation that spreadsheets struggle to handle consistently across multiple entities and reporting periods.

BrizoSystem addresses this directly:

Automatic balance matching: Intercompany loan receivables and payables are matched across entities based on counterparty and amount, flagging any differences before the elimination run begins.

Multi-currency support: FX differences on intercompany loans are calculated and allocated automatically — including the correct treatment for quasi-equity loans routed to the Currency Translation Reserve rather than the P&L.

NCI-aware eliminations: For partially owned subsidiaries, BrizoSystem applies eliminations at the correct ownership percentage and allocates the resulting profit impact between parent equity and NCI automatically.

Audit-ready documentation: Every elimination entry is logged with full drill-down to the originating loan balance, interest accrual, or FX adjustment — giving auditors the traceability they need without finance teams rebuilding the workings from scratch.

Recurring entry automation: Once elimination rules are defined for a loan, BrizoSystem applies them consistently in every subsequent period — so cash pooling arrangements with dozens of intercompany positions don’t require manual re-entry at each close.

Conclusion: Getting Intercompany Loan Eliminations Right

Intercompany loans and the interest they generate are among the most common — and most commonly mishandled — items in group consolidation. The mechanics of the elimination itself are straightforward, but the real complexity lies in the details: FX movements between reporting dates, quasi-equity classification decisions, NCI allocation, and timing mismatches across entities operating in different systems and time zones.

Getting these right is not just a compliance exercise. Accurate elimination of intercompany loans and interest directly affects the group’s reported leverage, interest coverage, and profitability — the metrics that lenders, investors, and boards rely on to assess financial health.

BrizoSystem is built to handle this complexity at scale — automating the matching, elimination, and allocation process so finance teams can close faster with confidence in every number.

👉 See how BrizoSystem handles intercompany loan eliminations → or See It in Action and walk through your group structure with our team.