When companies grow into multiple entities, transactions between those entities become inevitable. But when it comes time to prepare consolidated financial statements, these intercompany balances can distort the true financial picture. That’s where intercompany eliminations come in.

In this guide, we’ll walk through what intercompany eliminations are, the challenges finance teams face, the six most common types of eliminations with journal entries, and best practices to make the process smoother. For a deeper dive into balance sheet-specific entries — including goodwill, investment vs. equity, and contingent liability eliminations — see our Common Elimination Entries for Balance Sheet guide.

What Are Intercompany Eliminations?

Intercompany eliminations are adjustments made during the consolidation process to remove the effects of transactions between entities within the same group. If you’re new to the concept, our guide on why we eliminate intercompany transactions covers the reasoning and compliance requirements in full.

Under IFRS 10 – Consolidated Financial Statements and ASC 810 (US GAAP), eliminating intercompany transactions is a mandatory requirement — not an optional adjustment.

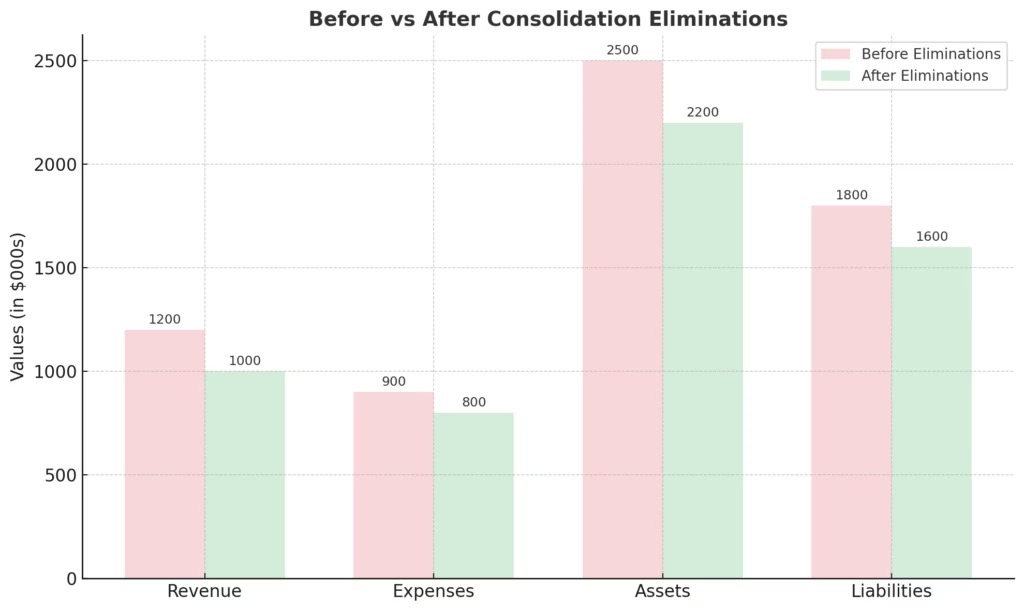

Without these eliminations, your consolidated financial statements would:

- Double-count revenues and expenses

- Inflate assets or liabilities

- Misrepresent the group’s overall performance

Example:

- Company A sells goods worth $100,000 to Company B (within the same group).

- If not eliminated, Group revenue would appear $100,000 higher than actual.

Common Challenges in Intercompany Eliminations

Even though the principle sounds simple—“remove intra-group transactions”—finance teams often face roadblocks:

- Data Silos Across Subsidiaries

Each entity may use a different accounting system (Xero, QuickBooks, MYOB, SAP, etc.), making it difficult to align data. - Multi-Currency Complexities

Transactions across currencies require careful FX translation. Timing mismatches in FX rates between entities often cause reconciliation issues. - Timing Differences

Subsidiary A records a sale in December, but Subsidiary B records the purchase in January. Without alignment, intercompany accounts won’t reconcile. - Inconsistent Coding

One entity books a transaction as “intercompany receivable,” while another books it under “accounts payable.” This lack of standardization complicates elimination. - Manual Processes

Heavy reliance on spreadsheets introduces errors, slows month-end close, and makes audits painful. - Unrealized Profits in Inventory or Assets

Eliminating only the transaction isn’t enough—profits embedded in intra-group inventory or assets also need adjustment.

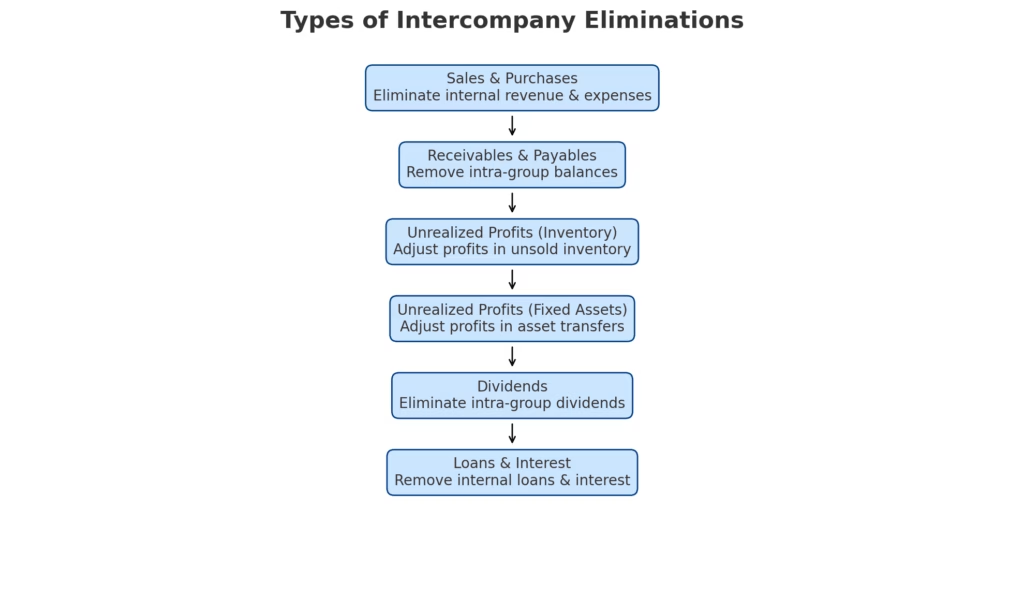

Types of Intercompany Eliminations

Intercompany eliminations cover different categories of intra-group activity. Each requires its own treatment.

1. Intercompany Sales & Purchases

Eliminating intercompany sales and purchases prevents the artificial inflation of group revenue and expenses. When one entity within the group sells to another, no real value is created for the consolidated group — it is simply a transfer of resources internally. If left unadjusted, consolidated revenue and costs will both be overstated by the value of those internal sales, misrepresenting the group’s true trading performance to shareholders, auditors, and lenders.

Example: Subsidiary A sells raw materials worth $500,000 to Subsidiary B. If left unadjusted, both consolidated revenue and cost of goods sold appear $500,000 higher than actual.

| Account | Debit | Credit |

|---|---|---|

| Revenue (Group) | $500,000 | |

| Cost of Goods Sold (Group) | $500,000 |

For a full step-by-step breakdown of how these entries are posted in practice, see our intercompany elimination process guide.

2. Intercompany Balances (Receivables & Payables)

When one entity records an intercompany receivable and another records the corresponding payable, these cancel each other out at consolidation. Leaving them in place would suggest the group owes money to itself — overstating both assets and liabilities with no economic substance behind them.

Example: Subsidiary A records a receivable from Subsidiary B for $200,000. Subsidiary B records the payable for the same amount.

| Account | Debit | Credit |

|---|---|---|

| Intercompany Payable (Subsidiary B) | $200,000 | |

| Intercompany Receivable (Subsidiary A) | $200,000 |

Timing mismatches — where one entity has recorded the transaction and the other hasn’t — are one of the most common causes of residual balances after elimination. These should be identified and resolved before the consolidation run, not after.

3. Unrealized Profits in Inventory

When goods are sold within the group at a profit but remain unsold to external customers at period end, that profit is unrealised from the group’s perspective. Recognising it would overstate both consolidated profit and inventory values. The correct elimination entry depends on when the profit originated.

Example: Subsidiary A sells inventory to Subsidiary B at a profit of $50,000. At year end, Subsidiary B still holds that inventory.

Current period (profit arose this period):

| Account | Debit | Credit |

|---|---|---|

| Cost of Sales | $50,000 | |

| Inventory (Subsidiary B) | $50,000 |

Prior period (profit arose in a previous period, inventory still held):

| Account | Debit | Credit |

|---|---|---|

| Retained Earnings (opening balance) | $50,000 | |

| Inventory (Subsidiary B) | $50,000 |

The distinction matters: debiting Cost of Sales applies when the unrealised profit arose in the current reporting period. Debiting Retained Earnings applies when it originated in a prior period and carried forward. Applying the wrong entry misstates both the income statement and opening equity.

4. Unrealized Profits in Fixed Assets

When one entity sells a fixed asset to another group entity at a gain, that gain is unrealised externally. Two adjustments are required: eliminating the gain itself, and correcting the depreciation the receiving entity has been charging — since it’s depreciating the asset at the inflated transfer price rather than the group’s original cost.

Example: Subsidiary A sells equipment to Subsidiary B at a gain of $100,000. Subsidiary B depreciates the asset over 5 years ($20,000/year at transfer price vs. $0 remaining on original cost).

Step 1 — Eliminate the unrealised gain:

| Account | Debit | Credit |

|---|---|---|

| Gain on Sale of Asset | $100,000 | |

| Fixed Assets — Net Book Value (Subsidiary B) | $100,000 |

Step 2 — Reverse excess depreciation (Year 1):

| Account | Debit | Credit |

|---|---|---|

| Accumulated Depreciation (Subsidiary B) | $20,000 | |

| Depreciation Expense | $20,000 |

Both entries are required every year until the asset is fully depreciated or sold externally. Applying only Step 1 corrects the balance sheet at acquisition date but leaves the income statement overstating depreciation expense each subsequent year.

5. Intercompany Dividends

When a subsidiary pays a dividend to its parent or another group entity, that payment is a movement of funds within the group — not income generated from external operations. If not eliminated, consolidated profit is overstated by income the group has effectively already recognised through the subsidiary’s retained earnings.

Example: Subsidiary A declares a $1,000,000 dividend to the Parent.

| Account | Debit | Credit |

|---|---|---|

| Dividend Income (Parent) | $1,000,000 | |

| Retained Earnings (Subsidiary A) | $1,000,000 |

If the dividend is declared but unpaid at period end, the receivable and payable balances must also be eliminated from the balance sheet. For a full guide including partial ownership and timing scenarios, see our intercompany dividend elimination post.

6. Intercompany Loans & Interest

Loans between group entities do not increase the group’s overall resources — they are internal reallocations of cash. Similarly, interest income for the lender and interest expense for the borrower are transfers within the group, not external financing costs. Both the loan balances and the interest flows must be eliminated.

Example: Parent lends Subsidiary $5,000,000 with annual interest of $250,000.

Eliminate the interest:

| Account | Debit | Credit |

|---|---|---|

| Interest Income (Parent) | $250,000 | |

| Interest Expense (Subsidiary) | $250,000 |

Eliminate the loan balances:

| Account | Debit | Credit |

|---|---|---|

| Intercompany Loan Payable (Subsidiary) | $5,000,000 | |

| Intercompany Loan Receivable (Parent) | $5,000,000 |

Best Practices for Intercompany Eliminations

Getting eliminations right is critical for accuracy, compliance, and speed. Here are best practices to follow:

1. Standardize Chart of Accounts Across Entities

The foundation of accurate intercompany eliminations is consistency in how transactions are recorded. If each subsidiary or entity uses its own chart of accounts, reconciling intercompany balances becomes unnecessarily complicated and prone to error. By implementing a standardized chart of accounts across the group, every intercompany transaction can be identified, coded, and tracked in the same way. This not only simplifies the elimination process but also improves transparency, reduces manual mapping work, and provides auditors with clearer, more reliable data.

- Use consistent coding for intercompany accounts.

- Set up dedicated intercompany accounts (not “miscellaneous”).

2. Centralize Policies & Procedures

A common challenge in consolidation is that each entity may apply different accounting policies or use varying procedures to record intercompany transactions. This creates inconsistencies that make eliminations harder to manage. Establishing centralized policies and clear documentation on how intercompany transactions should be recognized, valued, and reported ensures that all subsidiaries follow the same rules. For example, standardizing exchange rate sources or defining uniform cutoff dates for recording sales and purchases helps align the timing and valuation of transactions. This consistency greatly reduces reconciliation issues during consolidation.

- Document how each type of intercompany transaction should be recorded.

- Ensure all entities follow the same policy (e.g., same FX rate source, same cutoff dates).

3. Perform Regular Reconciliations

Waiting until year-end or quarter-end to reconcile intercompany accounts often leads to bottlenecks, last-minute adjustments, and stressful closing cycles. Instead, finance teams should adopt a practice of reconciling intercompany balances on a monthly or even more frequent basis. Regular reconciliations allow mismatches to be spotted and corrected early, rather than compounding into large discrepancies at year-end. This proactive approach builds confidence in the accuracy of group financials, speeds up the closing process, and provides management with reliable interim results throughout the year.

- Don’t wait until year-end. Reconcile intercompany balances monthly or even weekly.

- Use intercompany confirmation processes between entities to resolve mismatches early.

4. Leverage Technology for Automation

Manual eliminations performed in spreadsheets are time-consuming, error-prone, and difficult to audit. As a group grows and the volume of intercompany transactions increases, automation becomes essential. Consolidation software can apply elimination rules automatically, ensuring consistent treatment of recurring entries such as intercompany receivables, payables, or loan balances. Advanced systems also integrate directly with different accounting platforms (e.g., Xero, QuickBooks, MYOB), reducing data silos and providing a single source of truth. Automation frees finance teams from repetitive tasks, reduces risk of errors, and allows more time to be spent on analysis rather than data entry.

- Use consolidation software (like BrizoConsol) to apply elimination rules consistently.

- Automate recurring eliminations such as intercompany receivables/payables.

- Integrate with source systems (Xero, QuickBooks, MYOB, etc.) to reduce data silos.

5. Track Unrealized Profits Separately

One of the trickiest aspects of intercompany eliminations is dealing with unrealized profits in inventory and fixed assets. These adjustments often need to be reversed in subsequent periods when goods are sold externally or assets are depreciated. To avoid confusion, finance teams should maintain detailed schedules that track unrealized profits separately, including information on which entity recorded the profit, the type of transaction, and the expected reversal timeline. This level of granularity not only ensures accuracy but also provides a clear audit trail that supports transparency and compliance.

- Maintain schedules for intra-group profits in inventory and fixed assets.

- Automate reversals once goods are sold externally or assets are depreciated fully.

6. Audit Trail & Transparency

Strong governance requires that all elimination entries are traceable and well-documented. Maintaining a clear audit trail—complete with supporting documentation and references—helps auditors verify eliminations and strengthens the credibility of consolidated reports. Transparency also means avoiding opaque adjustments: every elimination should have a clear rationale and source. Whether through system-generated reports or structured documentation, building audit readiness into the elimination process reduces the risk of surprises during external reviews and builds trust with stakeholders.

- Ensure every elimination entry has documentation.

- Provide clear audit trails for regulators, auditors, and management.

7. Invest in Training & Alignment

Even with the right systems and policies in place, intercompany eliminations can only be effective if the people responsible for recording transactions understand their role. Training finance staff at the subsidiary level ensures they know how to properly code intercompany transactions, which accounts to use, and how to follow group-wide procedures. Regular workshops or internal knowledge-sharing sessions can reinforce alignment across entities. A culture of collaboration between local finance teams and group consolidation teams reduces friction, improves data quality, and ensures that eliminations are accurate from the start.

- Train finance teams in subsidiaries on proper coding and booking practices.

- Establish communication channels for intercompany queries and reconciliation.

How BrizoConsol Helps

The six challenges outlined earlier — data silos, FX complexity, timing differences, inconsistent coding, manual processes, and unrealised profit tracking — are exactly the problems BrizoConsol is built to solve.

Data silos across systems: BrizoConsol connects directly with Xero, QuickBooks, MYOB, and other accounting platforms, pulling entity-level data into a single consolidation environment without manual exports or mapping.

Multi-currency FX: Currency conversion and translation adjustments are handled within the platform automatically — including FX differences that arise when intercompany balances are recorded at different rates on each side.

Timing differences: BrizoConsol flags unmatched intercompany balances before the consolidation run begins, so timing mismatches are identified and resolved at source — not discovered after elimination entries are posted.

Inconsistent coding: A Common Chart of Accounts (CCOA) across all entities means every intercompany transaction is coded consistently, removing the reconciliation friction that comes from different entities using different account names for the same transaction type.

Manual processes: Elimination rules are defined once and applied automatically in every subsequent period — so recurring entries like intercompany receivables, loan balances, and dividend eliminations don’t need to be rebuilt from scratch each close.

Unrealised profit tracking: BrizoConsol maintains schedules for intra-group profits in inventory and fixed assets, tracking the period of origination and applying the correct elimination entry — and reversing it automatically when goods are sold or assets depreciated.

One client reduced their month-end close from 7 days to 2 days by automating intercompany eliminations with BrizoConsol.

Conclusion: From Manual Reconciliations to Strategic Analysis

Intercompany eliminations are the foundation of any consolidated financial statement that is accurate, compliant, and trustworthy. Done well, they give business leaders, investors, and auditors a clear view of what the group is genuinely earning, spending, and owning — with no internal noise distorting the picture.

Done poorly — or inconsistently — they create audit findings, inflate performance metrics, and erode confidence in the numbers.

The good news is that with the right process, the right policies, and the right tools, even complex multi-entity groups can close faster, eliminate more accurately, and spend less time reconciling and more time analysing.

BrizoConsol is purpose-built for exactly this — connecting your entities, automating your eliminations, and delivering board-ready consolidated reports without the manual overhead.

👉 See how BrizoConsol handles intercompany eliminations → or See It in Action and walk through your own group structure with our team.