Non-Controlling Interest (NCI) has always been one of the most technically demanding areas of group consolidation. Ownership percentages, goodwill calculations, P&L allocations, disposal accounting — and the requirement that every number traces back to an auditable acquisition history. Most firms either handle it manually in Excel or avoid it entirely until audit forces the issue.

BrizoConsol’s NCI module — available as a Pro Feature — automates the entire lifecycle: acquisition, ongoing P&L allocation, and loss-of-control disposal. No manual journals. No separate workpaper.

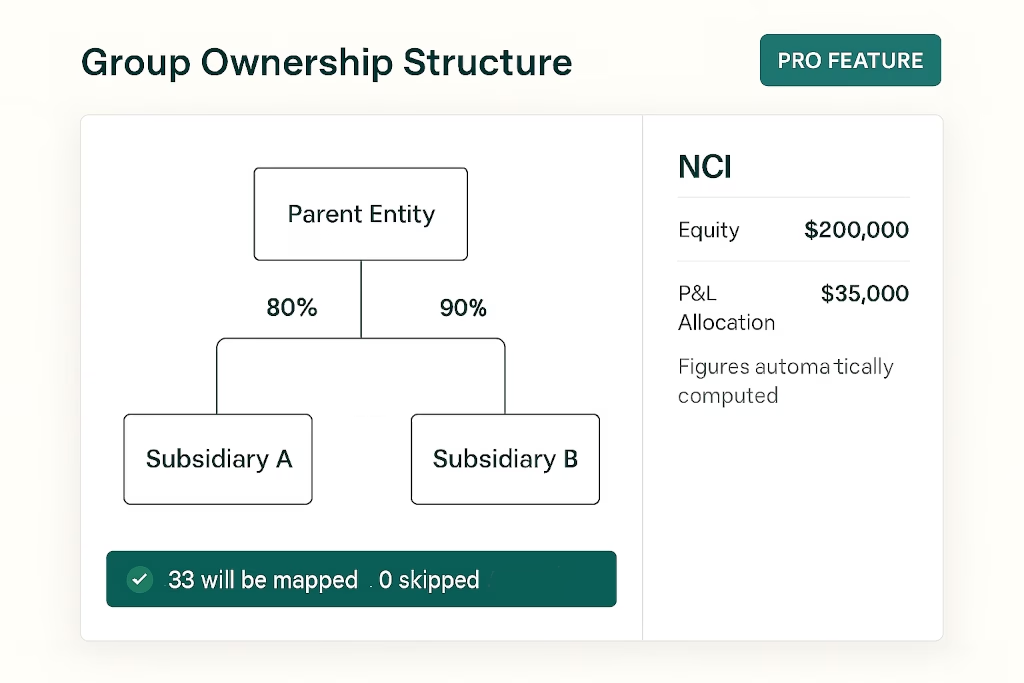

What Is NCI and Why Is It Technically Demanding?

When a parent company owns less than 100% of a subsidiary, the remaining ownership belongs to outside shareholders — the non-controlling interest. Under IFRS 10 and IAS 27, the group’s consolidated financial statements must:

- Present NCI as a separate component of equity (not as a liability)

- Allocate profit and loss between the parent and NCI based on ownership percentage each period

- Account for changes in ownership — additional stake acquisitions, partial disposals, and disposals that result in loss of control

- Calculate goodwill at acquisition date based on the difference between investment cost and the fair value of net assets acquired

Each of these steps involves precise, date-sensitive calculations that compound in complexity as ownership structures change over time. Getting any one wrong produces an auditable error that traces back to the original acquisition record. In Excel, maintaining this calculation chain correctly across multiple ownership changes — with the right period splits, the right goodwill anchor, and correct CTA allocation — is where most manual approaches eventually fail.

The NCI Module in BrizoConsol

Subsidiary-level NCI configuration

The NCI screen in BrizoConsol lists all eligible subsidiary entities with their key parameters visible in a single table. For each entity, the system shows the direct ownership percentage, the effective group percentage (accounting for intermediate parents), the resulting NCI percentage, whether NCI is enabled, and whether CTA is also active for the entity. A ready status confirms whether the entity is configured for the next consolidation run.

Below the entity list, the Ownership History tab records every ownership transaction in chronological order. Each row in the history drives the NCI percentage used in calculations — so BrizoConsol always knows the correct NCI percentage for every period, even if ownership has changed multiple times. The system calculates NCI automatically when the trial balance is resubmitted or when an ownership percentage changes. No manual trigger is needed.

Recording an acquisition — with goodwill calculated automatically

When the parent acquires a stake in a subsidiary, the transaction is recorded via the Add/Edit Ownership Record dialog. The required fields are straightforward: transaction type (Acquire or Dispose), the month of the transaction, the ownership percentage acquired, the investment cost, and — for the first acquisition in a subsidiary — the net assets at fair value at the acquisition date.

BrizoConsol uses the investment cost and the fair value net assets to derive goodwill automatically. For subsequent stake acquisitions, the system updates the effective group percentage and adjusts the NCI allocation accordingly — without requiring a separate goodwill recalculation.

How goodwill is calculated

First acquisition of a 90% stake: Investment cost $86,000 / Net assets at fair value $90,000

Goodwill = Investment cost − (Ownership % × Net assets at FV) = $86,000 − (90% × $90,000) = $86,000 − $81,000 = $5,000

NCI at acquisition = 10% × $90,000 = $9,000

No manual calculation required — BrizoConsol derives both from the acquisition record.

Disposal accounting — including loss of control

Disposal is where NCI accounting becomes most complex — and where most manual workflows break down. BrizoConsol’s Dispose transaction type handles it directly within the same Ownership Record workflow.

When a disposal drops cumulative parent ownership below 50%, BrizoConsol recognises this as a loss-of-control event and surfaces the additional required fields: the disposal proceeds, the retained interest fair value (required for remeasurement of the retained stake on loss of control), and the account to receive the retained interest fair value. A warning appears in the dialog confirming that cumulative ownership will fall below 50%, prompting configuration of the disposal gain/loss calculation before the transaction is confirmed.

🚩 Why loss-of-control disposal errors are so common: In a manual Excel consolidation, the point at which a partial disposal crosses the 50% threshold is often missed. The retained interest continues to be treated as a subsidiary when it should transition to the equity method, or the remeasurement of the retained stake at fair value is omitted. BrizoConsol catches this at the point of entry — not at audit.

What the NCI Engine Handles Automatically

Once ownership records are configured, BrizoConsol’s NCI engine handles:

- NCI equity allocation: The minority share of net assets is posted to consolidated equity automatically at each consolidation run

- P&L allocation: Profit and loss is split between parent and NCI based on the ownership percentage applicable to each period

- Goodwill calculation: Derived from investment cost versus net assets at fair value at the acquisition date; no manual workpaper required

- CTA on NCI: Where CTA is enabled for the entity, translation differences attributable to NCI are handled as part of the same consolidation run

- Post NCI Journal: One action posts the computed NCI entries to the consolidated statements, following the same Reconcile → Verify → Post workflow used across all BrizoConsol adjustment modules

Who This Is Built For

| Scenario | How the NCI module helps |

|---|---|

| Group with partially owned subsidiaries | Automatic NCI % calculation from ownership history — no manual percentage input each period |

| Multi-currency group with minority interests | CTA and NCI handled in the same consolidation run; NCI share of CTA allocated automatically |

| Ownership structure changed mid-year | Date-sensitive calculation from the ownership transaction log; correct NCI % applied per period |

| Subsidiary disposed below 50% ownership | Loss-of-control disposal accounting with retained interest remeasurement surfaced at the point of entry |

| Audit requiring goodwill workpaper | Goodwill auto-calculated from acquisition cost versus fair value; auditable from the ownership record |

A Pro Feature Built for Complex Groups

NCI is a Pro Feature in BrizoConsol — designed for accounting firms and group CFOs managing structures where partial ownership, acquisition history, and disposal accounting are part of the regular consolidation cycle. It sits alongside CTA, Auto Elimination, and Elimination Validation in the Adjustments module, so the entire consolidation workflow — including NCI — lives in one auditable platform.

From acquisition to disposal, BrizoConsol’s NCI engine handles the calculations so your team handles the review. Learn more or see it in action →