Latest blogs

-

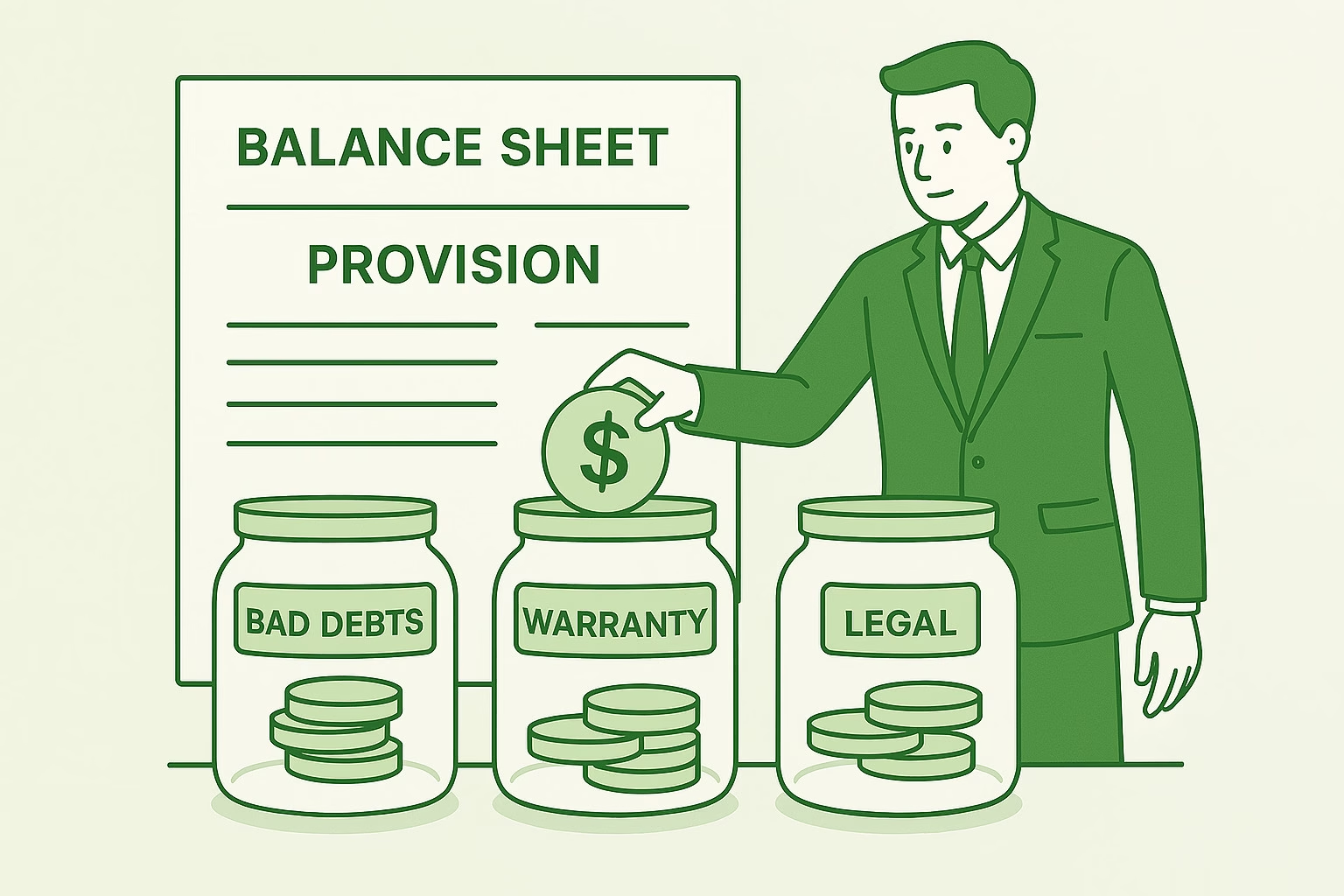

Understanding Provisioning in Accounting

A provision is a liability of uncertain timing or amount — recognised in the financial statements when a present obligation exists that will probably require a future outflow of resources and can be reliably estimated. Provisions sit at the intersection of the matching principle (recognise costs in the period they relate to) and prudence (don’t…

-

Foreign Currency Translation in Consolidation: Techniques and Best Practices

Foreign currency translation is the process of converting a foreign subsidiary’s financial statements from its functional currency into the group’s presentation currency so that they can be combined in the consolidated financial statements. The basic mechanics — balance sheet items at closing rate, P&L items at average rate, translation differences in OCI — are well-established…

-

Introducing BrizoConsol AI Assistants – Beta Launch!

We’re excited to announce the beta launch of BrizoConsol’s AI Assistants, designed to make financial management easier, faster, and more intuitive than ever. Our AI-powered helpers are ready to guide you, automate repetitive tasks, and provide insights — all from within BrizoSystem. Meet the BrizoConsol AI Team Each AI assistant is like a friendly robot…

-

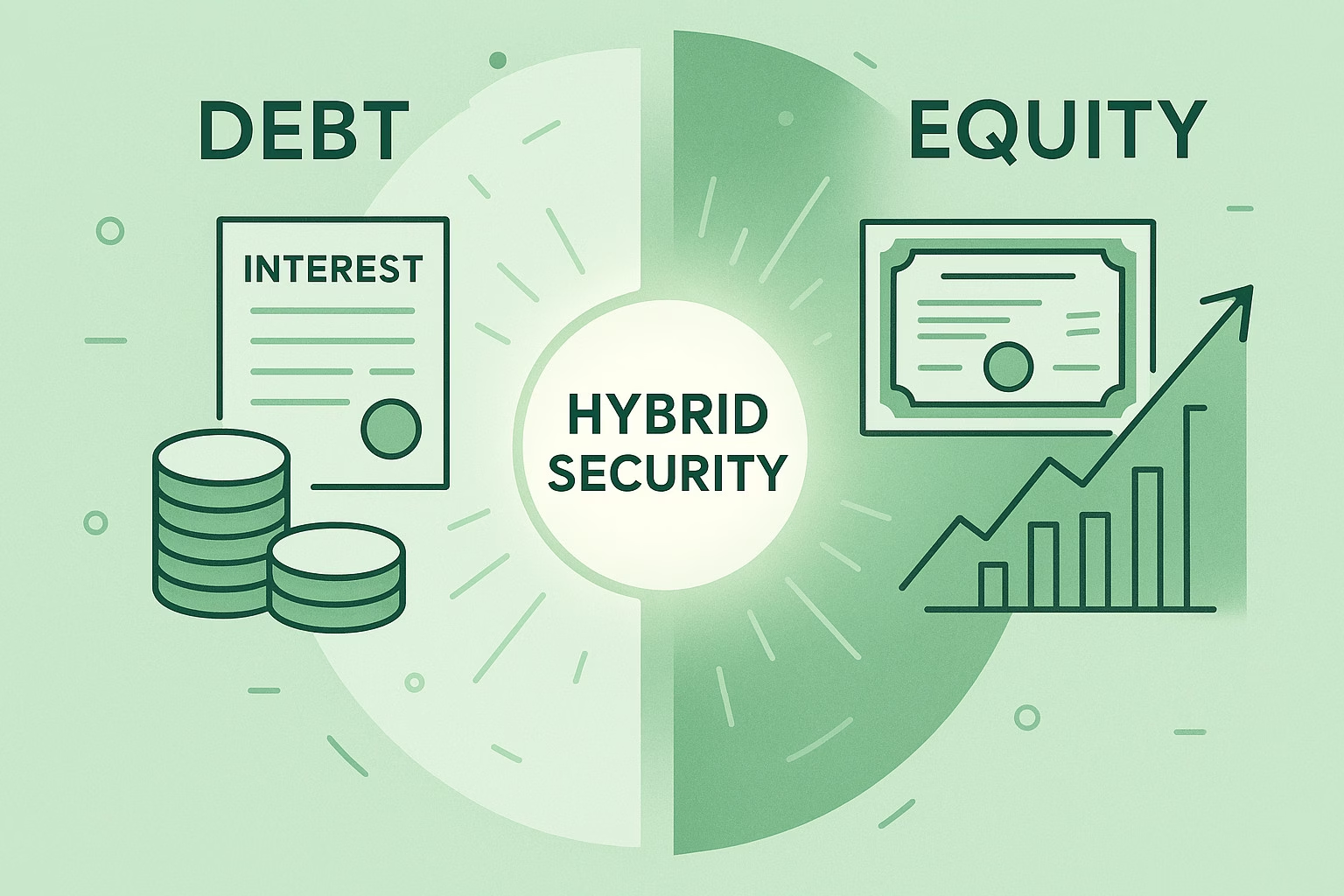

Understanding Hybrid Security Accounting

Hybrid securities combine debt and equity characteristics in a single instrument — convertible bonds, redeemable preference shares, perpetual subordinated notes, and similar instruments that don’t fit cleanly into either category. Their accounting classification under IAS 32 determines whether they appear on the balance sheet as a liability, as equity, or split into both components —…

-

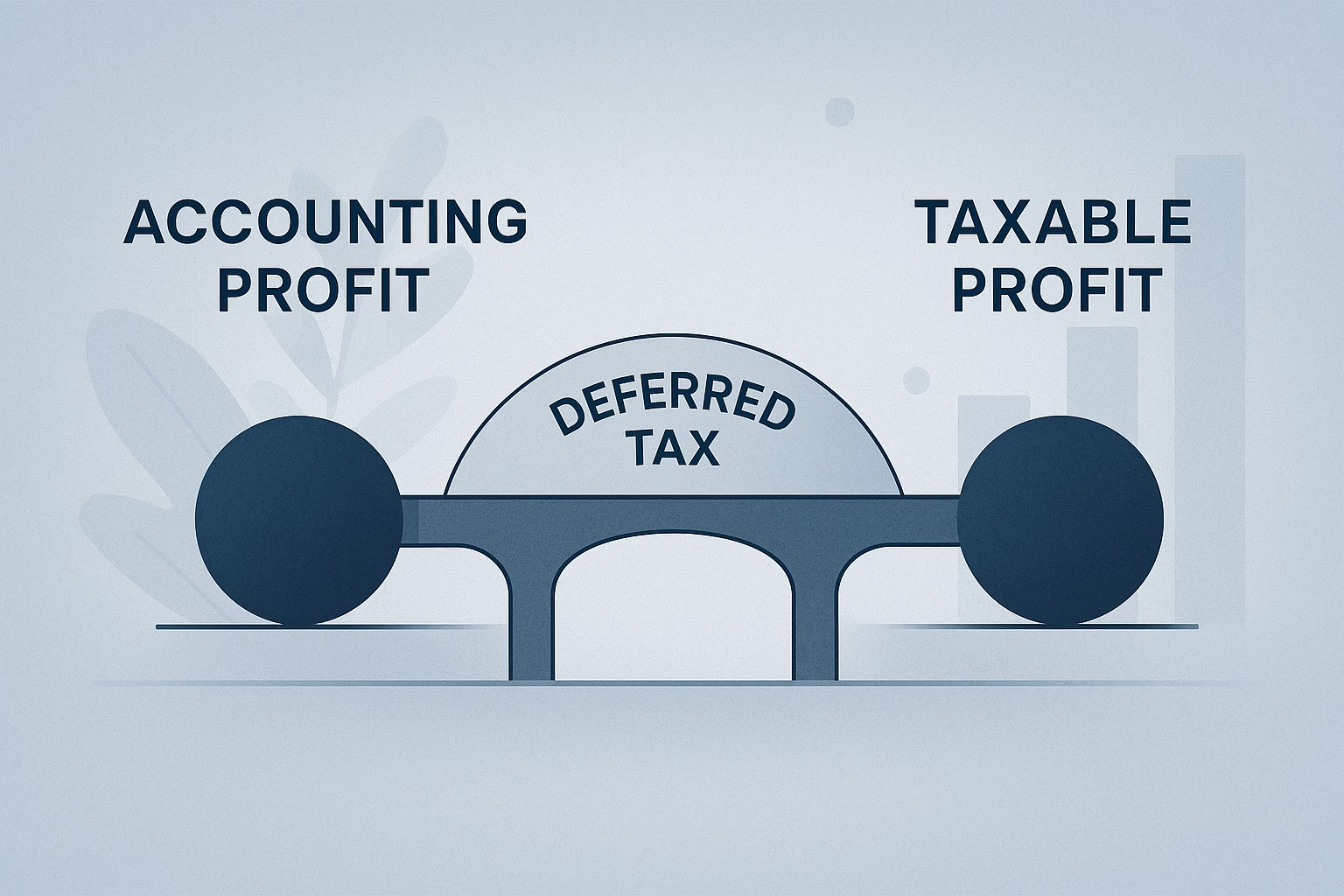

Deferred Taxes in Consolidation: Simplifying a Complex Accounting Area

Each entity in a group calculates its own deferred tax position — based on the temporary differences between its accounting carrying values and tax bases. These entity-level deferred taxes are aggregated into the consolidation. But the consolidation process itself also creates new deferred tax balances: temporary differences that don’t exist in any individual entity’s accounts…