Latest blogs

-

Understanding Contra Liability Accounts in Accounting

A contra liability account carries a debit balance — the opposite of a normal liability, which carries a credit balance. Rather than representing an amount the company owes, it reduces the carrying value of a related liability on the balance sheet, presenting a net figure that more accurately reflects the true economic obligation. Contra liability…

-

Intercompany Loans and Interest: Accounting, Elimination, and Common Mistakes

Intercompany loans are among the most common transactions in group structures and among the most reliably difficult to handle cleanly in consolidation. The basic elimination — remove the receivable in the lender, remove the payable in the borrower, remove the interest income and expense — is straightforward in principle. The complications arise from the variety…

-

Seamless Login Options Now Available: Xero & QuickBooks Integration

We’re excited to announce a new enhancement to BrizoConsol’s login experience — you can now log in using your Xero or QuickBooks accounts! What’s New? Previously, users logged in using their BrizoConsol credentials. With this update, you have more flexibility: This means no more juggling multiple passwords and an easier way to get started with…

-

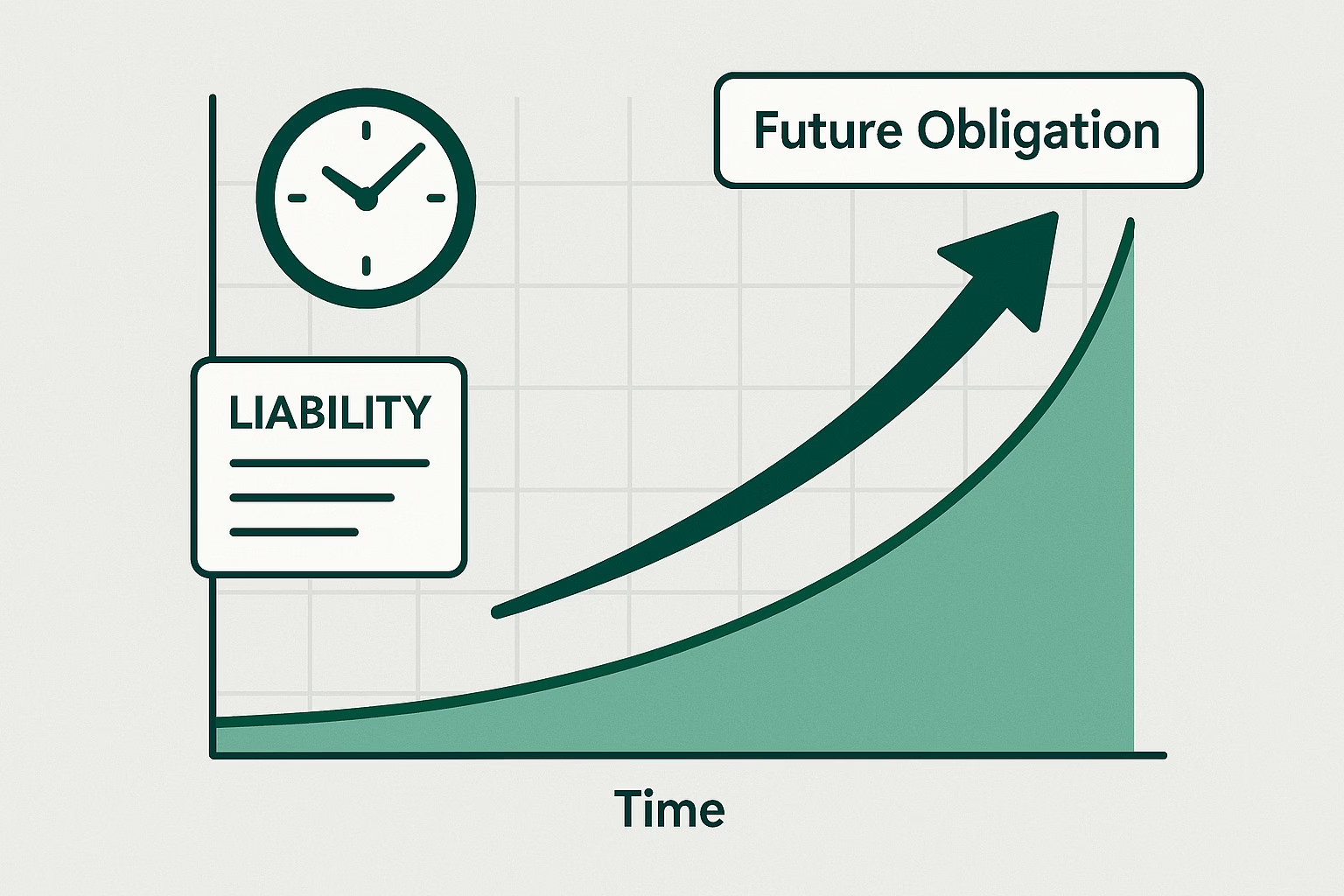

What is Accretion Expense?

Accretion expense is the periodic increase in the carrying amount of a discounted long-term liability as it approaches its settlement date. It arises because obligations that will be settled in the future are initially recorded at their present value — a figure lower than the actual amount that will ultimately be paid. As time passes,…

-

The Role of Consolidation in IFRS vs. US GAAP: Key Differences for Global CFOs

For groups that must navigate both IFRS and US GAAP — either because they operate across jurisdictions with different reporting requirements, or because they are preparing for a US listing while currently reporting under IFRS — the differences in consolidation rules are not only about accounting policies. They extend to which entities must be consolidated…