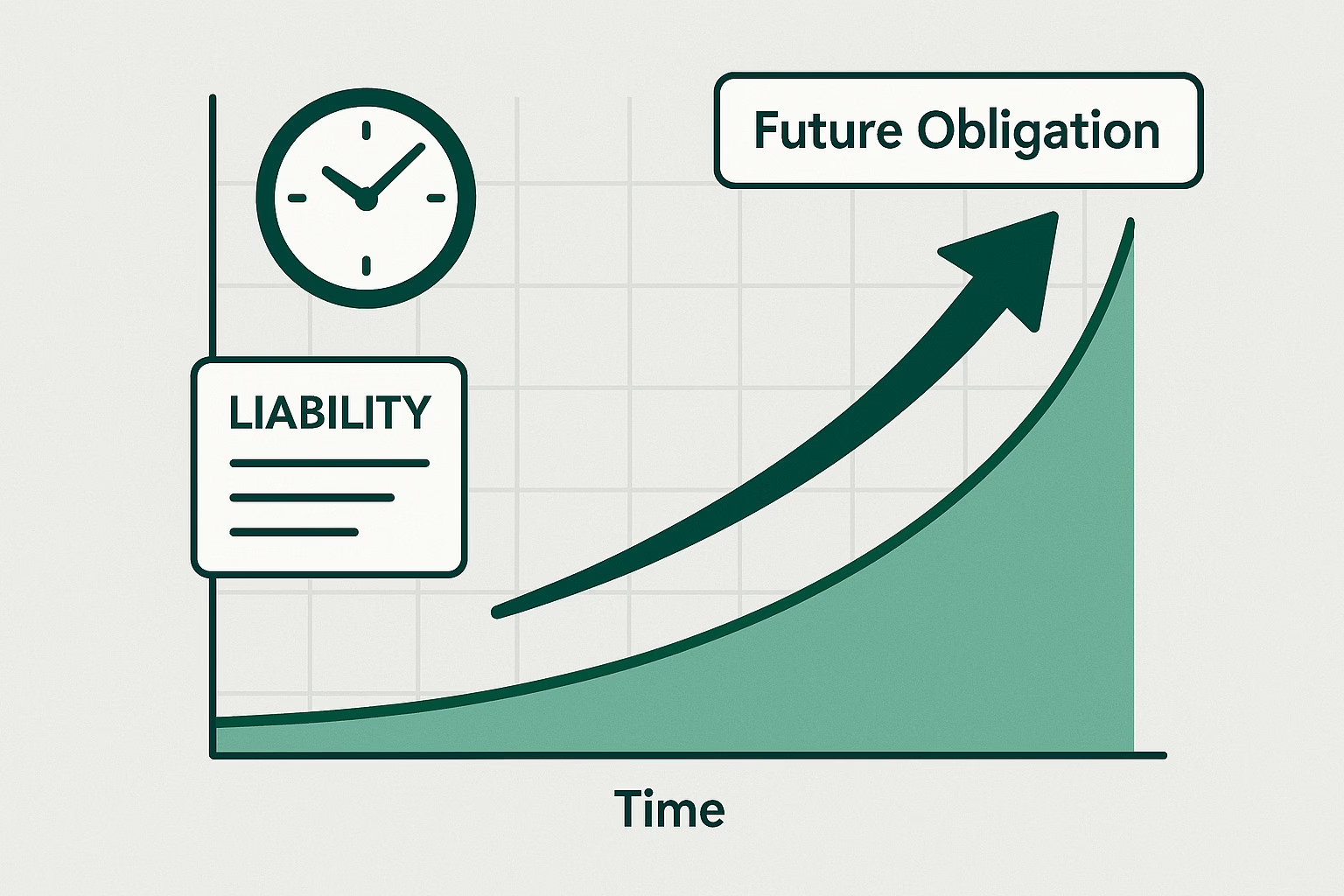

Accretion expense is an accounting term used to describe the gradual increase in the carrying amount of a liability over time. It represents the unwinding of a discount on long-term obligations — essentially, the cost of bringing a discounted future liability closer to its full value as time passes.

This concept is often applied in situations where a company has a future obligation that was initially recorded at its present value, such as:

- Asset retirement obligations (ARO) — e.g., the cost to dismantle an oil rig or restore land at the end of a project.

- Decommissioning liabilities in industries like mining or energy.

- Contingent liabilities recognized at discounted present values.

🧮 How It Works

When a company records a future obligation, it discounts the amount to present value using a suitable discount rate. Over time, as the settlement date approaches, that discount “unwinds” — meaning the present value grows to equal the actual future payment. This growth is recorded as accretion expense in the income statement.

Example:

- A company estimates it will pay $1,000,000 in 10 years to restore a site.

- The liability is discounted to $613,900 today using a 5% rate.

- Each year, the liability increases by 5% of its balance to reflect the passage of time.

| Year | Opening Liability | Accretion Expense (5%) | Closing Liability |

|---|---|---|---|

| 1 | 613,900 | 30,695 | 644,595 |

| 2 | 644,595 | 32,230 | 676,825 |

| … | … | … | … |

| 10 | … | … | 1,000,000 |

At the end of 10 years, the liability equals the actual payment due. Each year’s increase is the accretion expense — a non-cash charge representing the time value of money on the obligation.

💡 Why It Matters

- Financial accuracy – Ensures long-term obligations are reported at a realistic value.

- Expense recognition – Reflects the cost of time on discounted liabilities.

- Common in capital-intensive industries – Oil & gas, mining, utilities, and construction often report accretion expenses tied to asset retirement obligations.

🧾 Accounting Treatment

- Income Statement: Accretion expense is recorded as part of interest expense or a similar line item.

- Balance Sheet: The liability (e.g., asset retirement obligation) increases annually by the accretion amount.

- Cash Flow: Non-cash item, so it’s added back in the operating section when reconciling net income to cash flow.

🪙 In Simple Terms

Accretion expense is like interest on a future obligation — even though no cash leaves the company today, the cost of that liability grows steadily until payment is due.