Latest blogs

-

Who Sees What: A Guide to Role-Based Access and Team Collaboration in Group Financial Reporting

As finance teams grow, so does the complexity of managing access to financial data. What starts as a spreadsheet shared among a few people quickly becomes a governance problem when multiple entities, subsidiaries, external advisors, and stakeholders are involved — each with different information needs and different permissions to act on what they see. Not…

-

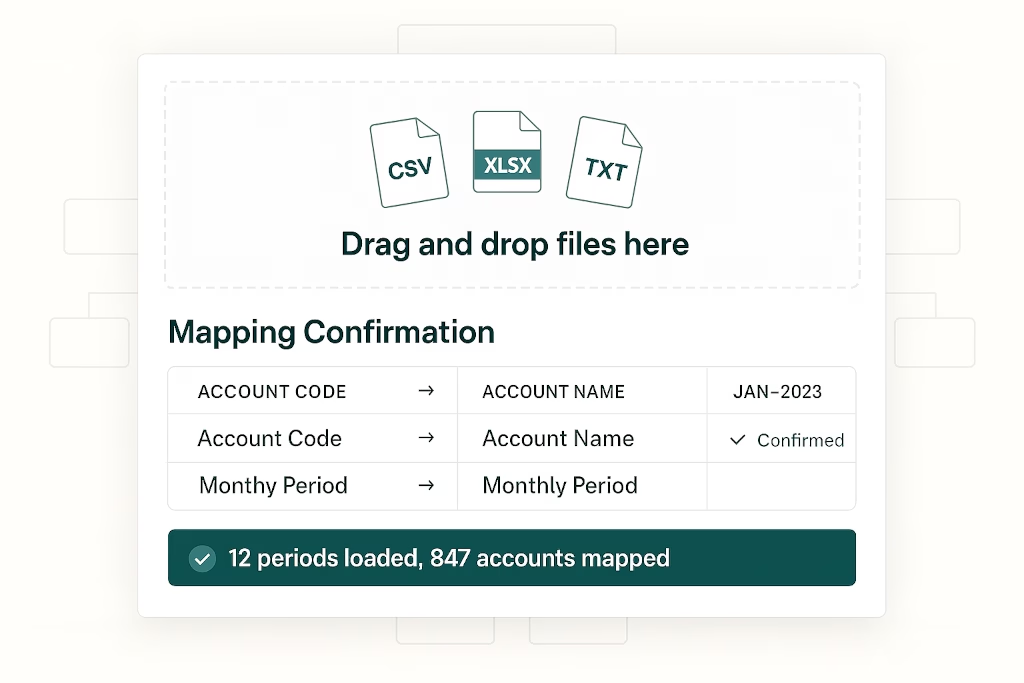

BrizoConsol Accepts Any Financial Export — Here’s Exactly How the Upload Works

Every accounting system exports data differently. Xero uses two-row headers. QuickBooks exports ledger detail. Some clients send a tidy monthly trial balance; others send a multi-sheet workbook with one period per tab. And then there’s the firm that emails a CSV with columns labelled “Period A,” “Period B,” “Q1.” BrizoConsol’s financial upload is built for…

-

Financial Consolidation for Holding Companies: A Practical Guide for CFOs and Finance Teams

Consolidation for a holding company group follows the same fundamental principles as any group consolidation — combine entity data, eliminate intercompany transactions, apply the right accounting standards. What makes holding company structures specifically interesting is the character of the holding company’s own accounts, and what happens to those accounts when they are consolidated with the…

-

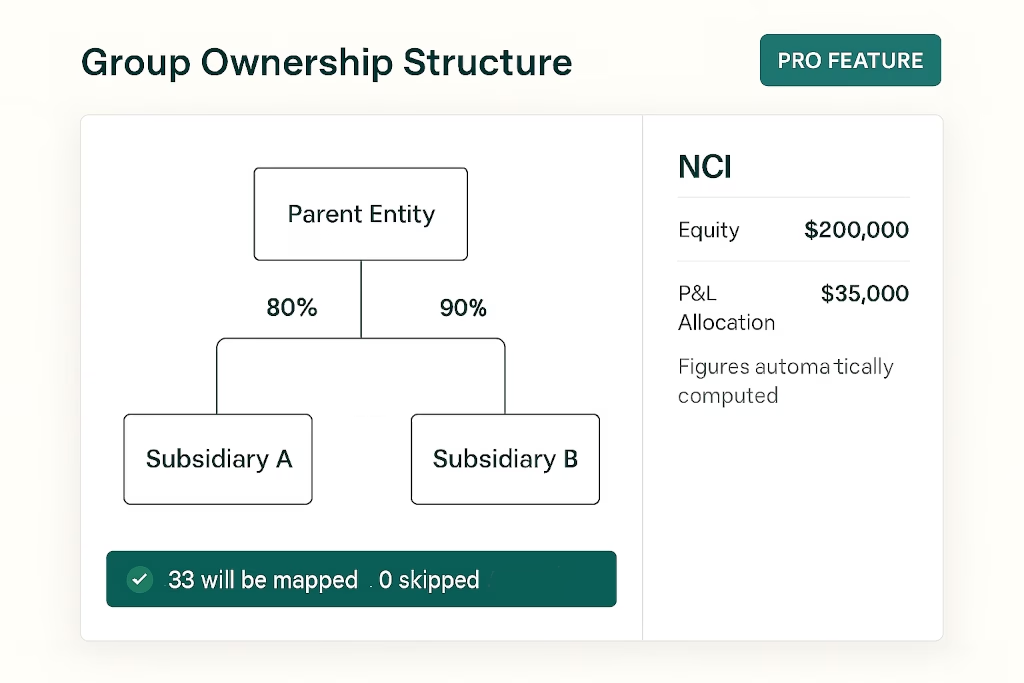

NCI, Fully Automated — Introducing Non-Controlling Interest in BrizoConsol

Non-Controlling Interest (NCI) has always been one of the most technically demanding areas of group consolidation. Ownership percentages, goodwill calculations, P&L allocations, disposal accounting — and the requirement that every number traces back to an auditable acquisition history. Most firms either handle it manually in Excel or avoid it entirely until audit forces the issue.…

-

Financial Consolidation for Franchise Groups: A CFO’s Guide to Clean Group Reporting

Financial consolidation for a franchise group is fundamentally different from consolidation in a standard corporate group — and the difference starts with a question that the consolidation must answer correctly before any technical work begins: which entities are actually part of the group? In a standard corporate group, all subsidiaries are owned by the parent…