If your group has subsidiaries operating in foreign currencies, you already know the pain. Three different exchange rates. Multiple equity accounts. Retained earnings accumulated over years at different rates. And a CTA balance in OCI that has to be mathematically perfect before you can close the consolidation.

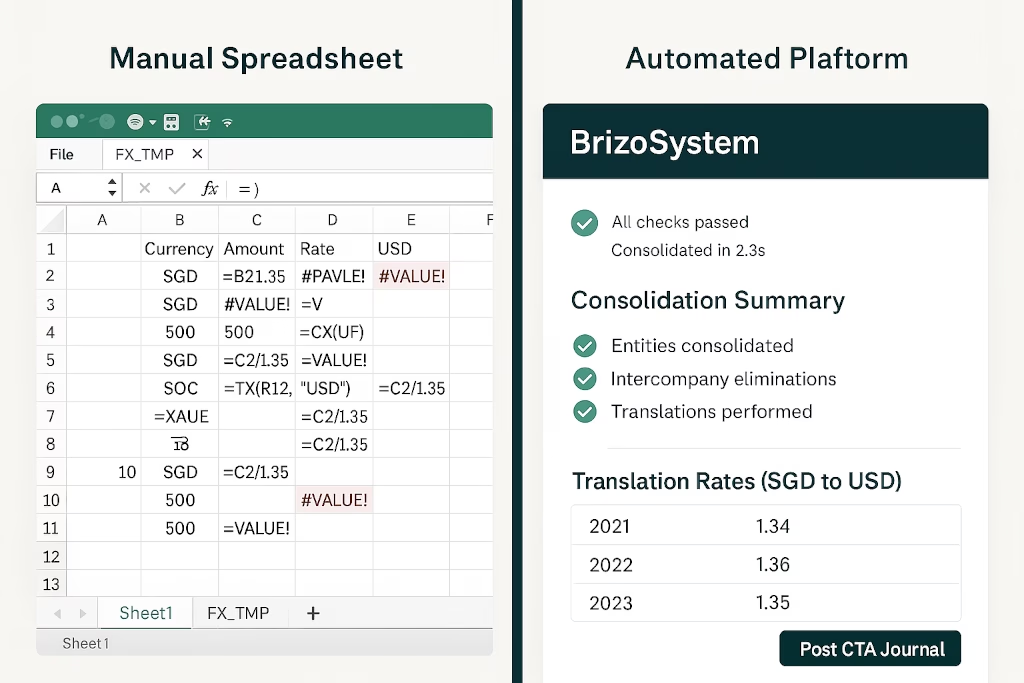

Most firms still do this in Excel. BrizoConsol eliminates it entirely.

What Is CTA and Why Does It Exist?

Under IFRS (IAS 21) and US GAAP (ASC 830), foreign subsidiaries must be translated into the group’s presentation currency using different rates for different account types:

- Closing rate — balance sheet assets and liabilities

- Average rate — income statement items

- Historical rate — equity accounts (share capital, reserves, retained earnings at acquisition)

Because these three rates are almost never the same, a mathematical gap always emerges between the translated balance sheet and the translated equity. That gap is the Currency Translation Adjustment — posted to Other Comprehensive Income (OCI), not the P&L. It doesn’t affect operating profit or cash, but it directly moves group equity and must be fully reconciled at every year-end.

Why CTA arises — simplified example A SGD subsidiary has net assets of SGD 1,000,000. Share capital of SGD 500,000 was contributed when the rate was 0.70 (historical rate). Retained earnings of SGD 500,000 accumulated at an average rate of 0.72.

Closing rate at year-end: 0.75

Balance sheet translated at closing rate: SGD 1,000,000 × 0.75 = USD 750,000

Equity translated at historical/average rates: (SGD 500,000 × 0.70) + (SGD 500,000 × 0.72) = USD 350,000 + USD 360,000 = USD 710,000

CTA = USD 750,000 − USD 710,000 = USD 40,000 posted to OCI

This gap is not an error — it is the arithmetic consequence of applying different rates to different account types. It must be calculated precisely and posted to OCI every year.

Why Equity Uses Historical Rates

The historical rate principle for equity reflects a specific accounting logic: share capital was contributed at a point in time, and its SGD value should be translated at the rate that applied at that moment — not the rate today. The same applies to reserves created at inception. Retained earnings accumulated across multiple years are translated at the average rate of each respective year, not the current closing rate.

This is where manual processes most commonly fail. A subsidiary operating for ten years has retained earnings accumulated across ten different annual average rates. Each year’s opening retained earnings must be rolled forward at the correct rate. Getting any single year wrong produces a cumulative error that grows over time and is extremely difficult to diagnose after the fact.

CTA Recycling on Disposal

When a foreign subsidiary is sold or otherwise disposed of, the accumulated CTA sitting in OCI is reclassified to the income statement — it is “recycled” to P&L as part of the gain or loss on disposal. This is required under IAS 21.48 and means the CTA balance must be tracked carefully at the entity level: the amount that gets recycled must match the amount that was accumulated in OCI over the life of the subsidiary.

If the accumulated CTA has been calculated imprecisely in prior periods — because rates were approximated or retained earnings were not translated year by year — the recycled amount will be wrong, producing a disposal gain or loss that does not accurately reflect the economics of the transaction.

NCI and CTA

For partially owned foreign subsidiaries, the CTA must be split between the parent’s share and the non-controlling interest’s share. The NCI is entitled to its proportion of the translation difference, just as it is entitled to its proportion of the subsidiary’s profit. In the consolidated SOCE (Statement of Changes in Equity), the CTA line must show both components — the parent’s CTA and the NCI’s CTA — separately.

This allocation is straightforward in principle but adds another layer of calculation that manual spreadsheets routinely get wrong when ownership percentages change during the period.

How BrizoConsol Handles CTA

BrizoConsol’s CTA module sits inside Adjustments → Automated in the consolidation workflow.

Configure per subsidiary — with full rate control

For each foreign subsidiary, BrizoConsol lets you define the functional and presentation currencies, toggle CTA on only for qualifying foreign operations, and set equity historical rates per account — Share Capital, Share Premium, Revaluation Reserve, Hedging Reserve, FVOCI Reserve, each mapped to its own historical rate.

Rates are sourced automatically by the system but can be overridden manually per account where needed. The Source column shows whether the rate is system-derived or manually set, giving you a clean audit trail on every line.

Retained earnings translated year by year

BrizoConsol handles the full retained earnings translation history automatically. Each year’s balance is translated at the correct yearly average rate, with the translated amount calculated and displayed instantly. In the example configuration for Demo Sales Company, four years of retained earnings — 2024 through 2027 — are each translated at their respective average rates (1.3265, 1.3445, 1.3310, 1.3310), with the source column confirming system vs manual override.

This removes what is typically the most manual, error-prone step in any multi-currency consolidation — and ensures the recycled CTA on disposal will be correct.

One click to post

Once configuration is complete, Reconcile / Verify CTA lets you review both auto and manual CTA journals before committing. When everything checks out, Post CTA Journal posts the balance directly into the consolidated financial statements — no manual journal entry required.

CTA posts at fiscal year-end and flows only into consolidated statements, not into the subsidiary’s standalone books. Exactly as it should be.

What This Replaces

| Manual process | BrizoConsol |

|---|---|

| Spreadsheet with hardcoded exchange rates | Centrally managed rates, applied automatically |

| Manual journal to post CTA to OCI | One-click Post CTA Journal |

| Separate retained earnings translation workpaper by year | Built-in Retained Earnings by Year tab |

| No audit trail on rate sources | System vs Manual source tracked per line |

| Risk of rate version mismatch across entities | Single source of truth across all subsidiaries |

| Manual CTA split between parent and NCI | NCI share of CTA allocated automatically |

Built for Accounting Firms Managing Multi-Entity Clients

If you run consolidated reporting for groups with offshore subsidiaries — whether in SGD, USD, GBP, AUD, or any other currency mix — BrizoConsol’s CTA module is built for exactly that workflow. It’s part of a complete consolidation engine that also handles auto eliminations, NCI, multi-line journal entries, and Elimination Validation — all in one platform.

See how BrizoConsol handles CTA, eliminations, and consolidated reporting end to end — without a spreadsheet in sight. Learn more or see it in action →