When consolidating financial statements, one crucial aspect is adjusting for minority interest, also known as non-controlling interest. Minority interest represents the portion of a subsidiary not owned by the parent company, reflecting the ownership held by outside shareholders. Properly accounting for minority interest ensures that consolidated financial statements accurately present the financial performance and position of the entire group.

What is Minority Interest?

Minority interest, or non-controlling interest, refers to the share of a subsidiary’s net assets and earnings attributable to shareholders other than the parent company. It arises when the parent company owns less than 100% of the subsidiary but still exercises control (typically through majority ownership of over 50%).

For example, if a parent company owns 80% of a subsidiary, the remaining 20% is considered minority interest. This minority stake must be recognized separately in the consolidated financial statements, ensuring that the interests of external shareholders are properly accounted for.

How NCI Is Measured at Acquisition

Under IFRS 3 – Business Combinations, there are two permitted methods for measuring NCI at the acquisition date. The choice between them affects both the goodwill recognised and the NCI balance carried on the consolidated balance sheet.

Method 1 — Proportionate Method (Share of Net Assets) NCI is measured as the minority shareholders’ percentage of the subsidiary’s identifiable net assets at fair value. This is the simpler approach and results in lower goodwill.

Example: Parent acquires 80% of Subsidiary for $900,000. Subsidiary’s net assets at fair value = $1,000,000.

- NCI (20%) = $1,000,000 × 20% = $200,000

- Goodwill = $900,000 − ($1,000,000 × 80%) = $100,000

| Account | Debit | Credit |

|---|---|---|

| Net Assets (Subsidiary — at fair value) | $1,000,000 | |

| Goodwill | $100,000 | |

| Investment in Subsidiary (Parent) | $900,000 | |

| Non-Controlling Interest | $200,000 |

Method 2 — Full Goodwill Method (NCI at Fair Value) NCI is measured at its fair value — typically based on the market price of the minority shares. This results in higher goodwill because it includes the goodwill attributable to the NCI as well as the parent.

Example: Same scenario, but minority shares are valued at $220,000 at acquisition.

- NCI (fair value) = $220,000

- Goodwill = ($900,000 + $220,000) − $1,000,000 = $120,000

| Account | Debit | Credit |

|---|---|---|

| Net Assets (Subsidiary — at fair value) | $1,000,000 | |

| Goodwill | $120,000 | |

| Investment in Subsidiary (Parent) | $900,000 | |

| Non-Controlling Interest | $220,000 |

Which method applies? IFRS 3 permits both methods and the choice can be made on a transaction-by-transaction basis. US GAAP (ASC 805) requires the full goodwill method only — NCI must always be measured at fair value. Groups reporting under both standards need to be aware of this difference when consolidating entities acquired under either framework.

Why is Minority Interest Important?

- Accurate Representation: Minority interest adjustments ensure that the consolidated financial statements accurately represent the interests of all shareholders, not just the parent company.

- Compliance with Accounting Standards: Both IFRS and GAAP require minority interest to be reported separately, making it a key compliance requirement for consolidated financial reporting.

- Reflects True Economic Control: By accounting for minority interest, consolidated financials reflect the actual economic control the parent has over its subsidiaries.

- Improves Transparency: Clearly showing minority interest enhances transparency for investors and stakeholders, providing a clearer picture of the group’s ownership structure and performance.

How to Account for Minority Interest

Minority interest is reported on the consolidated balance sheet within the equity section and is also reflected in the income statement as a share of profits attributable to minority shareholders. The key steps in accounting for minority interest include:

- Determine the Ownership Percentage:

- Identify the percentage of the subsidiary owned by the parent company and the percentage owned by minority shareholders.

- Calculate the Minority Interest in Net Assets:

- Minority interest is calculated as the minority shareholders’ percentage of the subsidiary’s net assets (assets minus liabilities).

- If the subsidiary’s net assets are $1,000,000 and the minority ownership is 20%, the minority interest in net assets would be: Minority Interest in Net Assets=$1,000,000 × 20% = $200,000

- Calculate the Minority Interest in Net Income:

- Minority interest in the income statement reflects the minority shareholders’ share of the subsidiary’s profits or losses.

- If the subsidiary reports a net income of $500,000, and the minority interest is 20%, the portion attributable to minority shareholders would be: Minority Interest in Net Income=$500,000 × 20% = $100,000

- Presentation in Consolidated Financial Statements:

- On the Balance Sheet, minority interest is shown under the equity section as a separate line item.

- On the Income Statement, it appears as an adjustment to net income, showing the portion attributable to non-controlling interests.

Post-Acquisition Journal Entry — Allocating Profit to NCI

Each reporting period, the subsidiary’s profit is split between the parent and the NCI based on ownership percentages. The NCI’s share is recognised in both the consolidated income statement and added to the NCI equity balance on the balance sheet.

Example: Subsidiary reports net profit of $500,000. Parent owns 80%, NCI owns 20%.

| Account | Debit | Credit |

|---|---|---|

| Profit attributable to NCI (Income Statement) | $100,000 | |

| Non-Controlling Interest — Equity (Balance Sheet) | $100,000 |

If the subsidiary declares a dividend, the NCI’s share reduces their equity balance:

| Account | Debit | Credit |

|---|---|---|

| Non-Controlling Interest — Equity | $40,000 | |

| Dividends Paid to NCI | $40,000 |

Adjusting for Minority Interest in Financial Consolidation

Step-by-Step Adjustment Process

- Consolidate 100% of the Subsidiary’s Financials:

- Include all the subsidiary’s assets, liabilities, income, and expenses in the parent company’s consolidated financial statements, even if the parent does not own 100%.

- Adjust for Intercompany Transactions:

- Eliminate intercompany sales, loans, and other transactions between the parent and the subsidiary to avoid double counting.

- Calculate Minority Interest in Net Assets:

- As demonstrated above, determine the minority shareholders’ share of the subsidiary’s net assets and record this amount on the balance sheet.

- Calculate Minority Interest in Net Income:

- Determine the share of the subsidiary’s profit or loss attributable to minority shareholders and adjust the consolidated income statement accordingly.

- Report Minority Interest Separately:

- Clearly present the minority interest amounts on the consolidated financial statements, distinguishing them from the parent’s ownership.

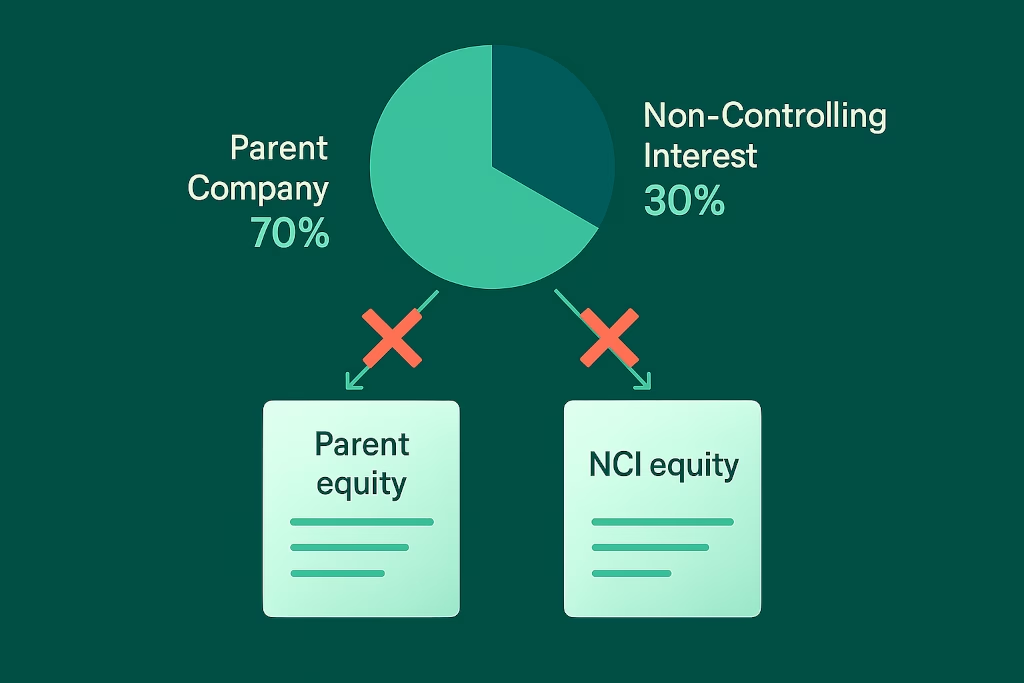

Example of Minority Interest Adjustment

Scenario:

- Parent Company A owns 70% of Subsidiary B. The subsidiary’s net assets are $2,000,000, and its net income for the year is $600,000.

Step 1: Calculate Minority Interest in Net Assets

- Minority ownership = 30%

- Minority Interest in Net Assets = $2,000,000 × 30% = $600,000

Step 2: Calculate Minority Interest in Net Income

- Minority Interest in Net Income = $600,000 × 30% = $180,000

Step 3: Presentation in Financial Statements

- On the balance sheet, $600,000 is recorded under the equity section as minority interest.

- On the income statement, $180,000 is deducted from the consolidated net income, showing the portion attributable to minority shareholders.

How NCI Affects Intercompany Eliminations

One of the most commonly misunderstood aspects of NCI accounting is how it interacts with intercompany transaction eliminations. The key rule is: only the group’s share of an intercompany profit is eliminated — the NCI’s share is left intact.

This applies to all elimination types where a partially-owned subsidiary is one of the transacting parties.

Example — Unrealised profit in inventory:

Parent owns 75% of Subsidiary A. Subsidiary A sells inventory to another group entity at a profit of $80,000. At period end, all inventory remains unsold externally.

- Group’s share to eliminate: $80,000 × 75% = $60,000

- NCI’s share (remains): $80,000 × 25% = $20,000

| Account | Debit | Credit |

|---|---|---|

| Cost of Sales | $60,000 | |

| Inventory | $60,000 |

The remaining $20,000 stays in the consolidated accounts as it belongs to the minority shareholders — eliminating 100% would overstate the adjustment and misrepresent the NCI’s economic interest.

Example — Intercompany interest:

Parent owns 70% of Subsidiary B and charges it $100,000 in interest on an intercompany loan. After eliminating the interest, Subsidiary B’s profit increases by $100,000. The NCI (30%) is entitled to their share of that increase:

- Additional NCI allocation = $100,000 × 30% = $30,000

This must be reflected as an increase to the NCI equity balance — otherwise the elimination entry understates NCI and overstates parent equity.

Challenges in Accounting for Minority Interest

Accurate Valuation of Subsidiary Net Assets

NCI is calculated as a percentage of the subsidiary’s net assets — but those assets must be measured at fair value at the acquisition date, not book value. For subsidiaries with significant intangible assets, property portfolios, or complex financial instruments, fair value can be materially different from carrying value. Any misstatement in the fair value assessment flows directly into both goodwill and the NCI balance, affecting every subsequent period’s calculations.

Partial Elimination Errors

As shown above, intercompany eliminations in partially-owned subsidiaries require careful proportional treatment. Eliminating 100% when only the group’s share should be eliminated is one of the most common consolidation errors — and one of the hardest to spot in a manual process because the balance sheet still balances, just with the wrong split between parent equity and NCI.

Currency Translation for Foreign Subsidiaries

When a partially-owned subsidiary operates in a different functional currency, exchange rate movements affect the NCI balance as well as the parent’s share. Under IAS 21, the NCI’s share of currency translation differences is allocated within equity — but ensuring this split is calculated and presented correctly at each period end requires careful tracking, particularly in groups with multiple foreign subsidiaries each at different ownership percentages.

Changes in Ownership Percentage

If the parent acquires additional shares in a subsidiary (increasing ownership) or disposes of a portion (reducing ownership) without losing control, this is treated as an equity transaction — no gain or loss is recognised in the P&L, and the NCI balance is adjusted accordingly. Getting this right requires a precise calculation of the difference between the consideration paid/received and the NCI book value transferred, with any difference taken to parent equity. This is frequently handled incorrectly in manual consolidations.

Best Practices for Managing Minority Interest Adjustments

- Automate with Financial Consolidation Software: Use tools like BrizoConsol to automate the consolidation process, including the calculation of minority interests, intercompany eliminations, and currency adjustments.

- Standardize Reporting Procedures: Ensure all subsidiaries follow consistent accounting policies to streamline the consolidation and minority interest adjustments.

- Regularly Review Minority Interest Calculations: Periodically assess the valuation of subsidiaries and ensure that minority interest is accurately reflected in the consolidated statements.

- Train Finance Teams on Compliance Requirements: Ensure that finance teams are well-versed in the relevant accounting standards (IFRS, GAAP) and understand the intricacies of minority interest adjustments.

How BrizoConsol Handles NCI

Managing minority interest manually — across multiple partially-owned subsidiaries, different currencies, and changing ownership percentages — is one of the most calculation-intensive parts of group consolidation. Each period requires recalculating NCI balances, applying partial eliminations at the correct percentage, allocating profit splits, and tracking currency translation movements on the NCI equity balance.

BrizoConsol handles this within its consolidation engine:

Ownership structure management: Define each subsidiary’s ownership percentage once. BrizoConsol applies it automatically to profit allocations, NCI equity movements, and partial elimination calculations at every close — without manual recalculation.

Partial elimination support: For intercompany transactions involving partially-owned subsidiaries, BrizoConsol eliminates only the group’s proportionate share and correctly preserves the NCI portion — removing the risk of the most common NCI elimination error.

Multi-currency NCI tracking: Currency translation differences on NCI balances are calculated and allocated within equity automatically, in line with IAS 21 requirements.

Full audit trail: Every NCI adjustment is logged with its source calculation, ownership percentage applied, and period — giving auditors complete traceability without finance teams rebuilding the workings from scratch.

Conclusion: Getting NCI Right Matters More Than It Looks

Minority interest — or non-controlling interest — is not just a line item on the balance sheet. It affects how profits are split, how intercompany eliminations are applied, how goodwill is calculated, and how currency movements are allocated across equity. Errors in NCI accounting ripple through every part of the consolidated financial statements.

Done correctly, NCI accounting gives every stakeholder — parent shareholders, minority shareholders, lenders, and auditors — an accurate picture of who owns what and who earned what within the group.

As group structures become more complex — more subsidiaries, more currencies, more partial ownership arrangements — managing NCI manually becomes increasingly difficult to do consistently and defensibly.

BrizoConsol is built to handle this complexity, giving finance teams a structured environment to manage NCI calculations, partial eliminations, and equity movements with full visibility and audit-ready documentation at every reporting period.

👉 See how BrizoConsol handles NCI in consolidation → or See It in Action and walk through your own group ownership structure with our team.